|

Transform the APR to a decimal (APR% divided by 100. 00). Then calculate the rate of interest for each payment (because it is a yearly rate, you will divide the rate by 12). To calculate your regular monthly payment amount: Rate of interest due on each payment x quantity obtained 1 (1 + Rates of interest due on each payment) Variety of payments Presume you have actually looked for a car loan for $15,000, for 5 years, at an annual rate of 7. 20% Variety of payments = 5 x 12 = 60 Rates of interest as a decimal = 7. 20% 100 =. 072 Interest due on each payment =. 006 Plug each into above: =. 006 x $15,000 1 (1 +. 006) 60 To Determine Overall Finance Charges to be Paid: Regular Monthly Payment Amount x Variety Of Payments Amount Borrowed = Total Quantity of Finance Charges Plug each of the above into above: $298. 44 x 60 $15,000. 00 = $2,906. 13 The figures for a home loan will typically be a fair bit greater, but the fundamental solutions can still be utilized. We have a comprehensive collection of calculators on this site. You can utilize them to figure out loan payments and create loan amortization sheets that break out the part of each payment that goes to primary and interest over the life of a loan. A finance charge is the total quantity of money a customer spends for borrowing money. This can include credit on a vehicle loan, a credit card, or a home loan. Common financing charges include rates of interest, origination charges, service fees, late charges, and so on. The overall financing charge is normally related to charge card and includes the unsettled balance and other fees that use when you bring a balance on your credit card past the due date. A financing charge is the cost of obtaining cash and applies to different types of credit, such as automobile loans, home mortgages, and credit cards. A total financing charge is typically connected with credit cards and represents all costs and purchases on a charge card declaration. A total finance charge may be calculated in a little various methods depending upon the charge card business. At the end of each billing cycle on your charge card, if you do not pay the statement balance in complete from the previous billing cycle's statement, you will be charged interest on the overdue balance, as well as any late charges if they were incurred. How to finance a second home. Your financing charge on a credit card is based upon your interest rate for the kinds of transactions you're bring a balance on.

Your total financing charge gets contributed to all the purchases you makeand the Homepage grand overall, plus any fees, is your monthly charge card bill. Credit card companies calculate finance charges in various methods that lots of customers might discover confusing. A typical method is the typical day-to-day balance method, which is calculated as (typical everyday balance annual percentage rate variety of days in the billing cycle) 365. To compute your typical everyday balance, you need to look at your charge card statement and see what your balance was at completion of every day. (If your charge card declaration does not reveal what your balance was at the end of every day, you'll need to compute those quantities too.) Add these numbers, then divide by the number of days in your billing cycle.

Facts About How To Import Stock Prices Into Excel From Yahoo Finance Revealed

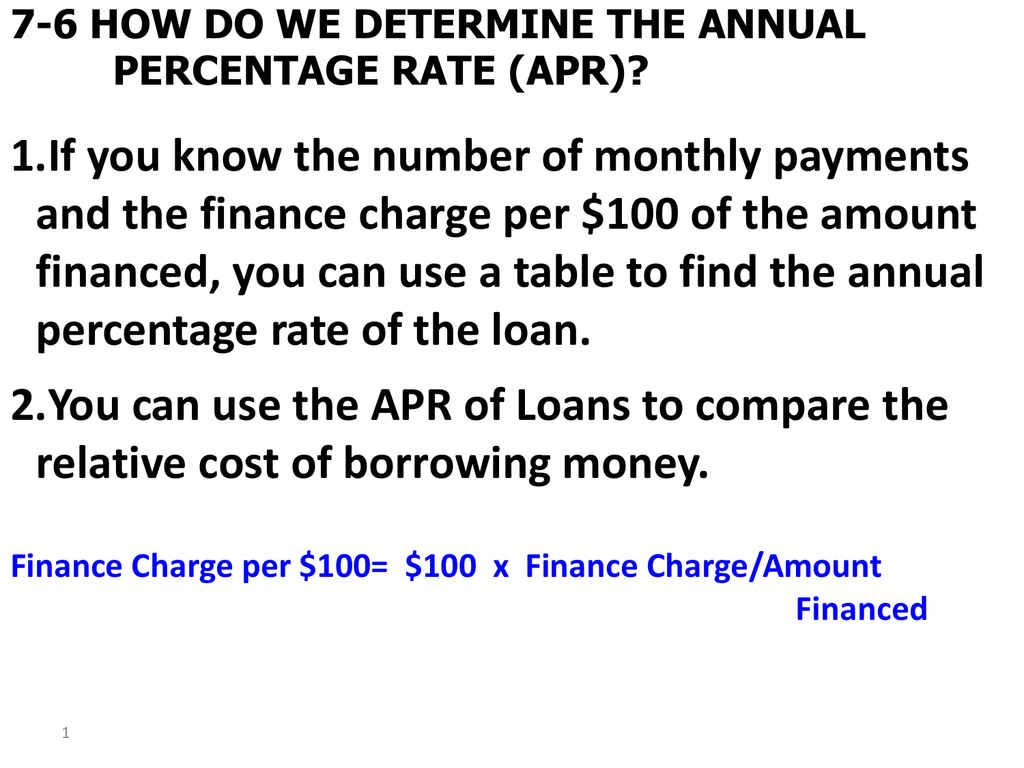

Wondering how to determine a financing charge? To offer an oversimplified example, suppose your everyday balances were as follows in a five-day billing cycle, and all your deals are purchases: Day 1: $1,000 Day 2: $1,050 Day 3: $1,100 Day 4: $1,125 Day 5: $1,200 Total: $5,475 Divide this overall by 5 to get your average day-to-day balance of $1,095. The next step in computing your total financing charge is to examine your credit card statement for your rate of interest on purchases. Let's say your purchase APR is 19. 99%, which we'll round to 20% (or 0. 20) for simpleness's sake. ($ 1,095 0. 20 5) 365 = $3 = Overall finance charge Your total finance charge to obtain an average of $1,095 for 5 days is $3. That does not sound so bad, however if https://pbase.com/topics/patric60el/eddhhri076 you carried a similar balance for the entire year, you 'd pay about $219 in interest (20% of $1,095). That's a high expense to borrow a small amount of cash. On your charge card statement, the total finance charge might be noted as "interest charge" or "finance charge." The typical day-to-day balance is simply one of the calculation approaches used. There are others, such as the adjusted balance, the daily balance, the double billing balance, the ending balance, and the previous balance. Installment purchasing is a kind of loan where the principal and and interest are settled in regular installments. If, like the majority of loans, the month-to-month quantity is set, it is a set installation loan Credit Cards, on the other hand are open installation loans We will concentrate on repaired installation loans for now. Generally, when acquiring a loan, you must offer a down payment This is usually a percentage of the purchase rate. It minimizes the quantity of money you will obtain. The quantity financed = purchase cost - deposit. Example: When acquiring a used truck for $13,999, Bob is required to put a deposit of 15%. Deposit = $13,999 x. 15 = $2,099. 85 Amount funded = $13,999 - $2099. 85 = $11,899. 15 The total installation cost = total of all monthly payments + down payment The finance charge = overall installment rate - purchase rate Example: Problem 2, Page 488 Purchase Rate = $2,450 Deposit = $550 Payments = $94. 50 Variety of Payments Get more info = 24 Discover: Amount funded = Purchase price - down payment = $2,450 - $550 = $1,900 Total installment price = total of all month-to-month payments + down = 24 months x $94. 50/month + $550 = $2,818. 5 page 482 shows the relationship in between APR, financing charge/$ 100 and months paid. You will need to understand how to utilize this table I will provide you a copy on the next test and for the last. Provided any two, we can find the third Example Number 6. Months = 18 Financing Charge/ $100 = 12. 72 Discover the APR: APR = 15. 5% APR is the yearly percentage rate for the loan. Months paid is self obvious. Financing charge per $100 To discover the finance charge per $100 offered the finance charge Divide the financing charge by the number of hundreds borrowed.

0 Comments

If you do fail to make your payments, your unaltered land is less appealing than residential or commercial property that can go to foreclosure auction. Land loans tend to come with greater rates of interest and more strict deposit and credit requirements than other kinds of home loans because of these threats to the lender. The terms of your land loan will depend on the type of loan you get, your prepare for the land and the particular lender you work with. In general, there are three types of land that lenders will think about financingraw, unimproved and improved landall of which feature their own advantages and disadvantages. There's no plumbing, electrical energy or access to close-by roads. Basically, it's a blank slate for you to deal with. Not surprisingly, raw land tends to be less expensive than developed land, however know that it might cost you more in the long run. Buying raw land is a risky possibility to lenders, so they typically compensate by charging greater rates of interest and needing greater down payments. In reality, you might need to put down 50% or more if the purchase is speculative, suggesting you are hoping residential or commercial property worths will rise. Click here for more Similar to many kinds of loans, a good credit rating and solid deposit will assist you get https://zenwriting.net/cechinnijp/at-this-moment-you-wouldand-39-ve-ideally-paid-off-your-very-first-mortgage approved for a raw land loan and receive the very best terms (What does ltm mean in finance). Next is unimproved land, which is rather open up to interpretation and sometimes associated with raw land. Typically, though, unimproved land describes land that has access to some basic utilities, but is still lacking major items such as an electric meter, phone box or natural gas meter. In other words, there are few added improvements to the plot. It might be a bit much easier to receive an unimproved land loan over a raw land loan, but it's still thought about dangerous. Once again, you should have a strong credit report, deposit and strategy for the land. Enhanced land The original source is the most costly choice given that it's completely developed and construction-ready. Some Of What Does Ach Stand For In Finance

Once you've conserved up a deposit, developed plans for your land and have a solid credit rating, it's time to look around for lenders. Land loans aren't as easy to come by as home loans, but you do have a number of options. One of the finest locations to search for a land loan is your neighborhood bank or cooperative credit union. Regional banks will have an excellent concept of how the surrounding land can be utilized and have more versatility when it comes to working with customers. The USDA supplies land loans to customers who plan to build a primary home in a rural location. Bigger advancement jobs can be financed if you have a strong possession position. Some lending institutions do not need evidence of earnings if you prepare to offer the residential or commercial properties on conclusion. You can obtain up to 70% of the Gross Realisation Worth (GRV) or 80% of the difficult costs. No presales are required for little duplex, townhouse and unit advancements. You may refinance your job on conclusion with a standard investment loan or low doc loan and keep a few of the homes. If you 'd like our assistance to fund your project, then please call us on or fill in our free evaluation kind and one of our home mortgage brokers will help you in applying to ensure that you get approval! We can assist you finance a job of as much as four residences, with a maximum loan amount of $1,500,000.

You can obtain approximately the lower of 70% of the Gross Realisation Worth (GRV) or 80% of the difficult expenses (value of land plus expense of construction only). We can't assist you with construction financing if you require a low doc owner contractor loan unless you are a builder. However, we can organize a low doc loan for as much as 80% of the land worth (not the on conclusion value) in addition to 80% of the value of any other residential or commercial properties that you own. Once your property is total, we can then increase your low doc loan to 80% of the worth of your property. You should look for the loan either before you start building or when the building is finished. Nevertheless, if you require additional funds throughout construction we can help you in the following situations: We can provide up to 60% of the overall expense. 75% of the overall cost. 80% of the overall expense (How to find the finance charge). The above loan quantities should be enough to pay your existing home mortgage and complete the building of your residential or commercial property. There are no exceptions to the above Loan to Value Ratios (LVRs). Please call us on or enquire online and we can assist you in obtaining the funds you require to complete your job. What Is The Reconstruction Finance Corporation - Questions

If you have a good friend or household member that can guarantee your loan then you might be able to obtain more than 80% of the task expense and as much as a maximum of 100% on a case by case basis. To learn more, please refer to our no deposit guarantor loan page. Basic guarantor loans aren't available so you'll need to make an application for an 80/20 guarantor loan. This is where the guarantor secures a home loan on their home and after that lends this to you to make up the difference between your 80% home mortgage protected by your property and the amount that you require to finish the task. We can make the application process less difficult for you! Unlike a traditional mortgage, the lender won't pay you all of the loan funds when the loan is setup. Instead, they'll launch funds to you as construction advances. This is referred to as 'development payments' or 'building and construction draw downs'. When you have actually completed each action of building, a bank valuer will be sent out to assess your work, validate you have actually followed the floor strategies and then authorise the bank to make the next payment. If you have significant equity offered in your land then we may have the ability to set up a credit line based on the value of your land alone. Roofing replacements can cost between $3,000 and $10,000. (Talk to an expert to get a more precise expense since complex roof tasks might cost more than $10,000). Most DIY roofing system repair work are most likely too cheap for an individual loan; brand-new asphalt shingles can cost a couple hundred dollars. You might wish to check out 0% APR credit cards for these jobs (What does leverage mean in finance). However for major, multi-thousand dollar roof repairs, an individual loan could be the best option for you. If you're attempting to get your home on the market, having a brand-new roofing might assist you close much faster. Personal loans might be a great suitable for this kind of upgrade. Even if your insurance coverage will cover your roofing, you may require a roofing replacement loan simply to cover the deductible. Not set on a personal loan? Continue reading to find out about other roof funding options. Note: If you're a roofing professional, visit our contractor funding page for more information about our funding program. You can likewise visit our partners at Roof Insights for other roofing pointers. You have actually been intending on changing your roofing, repairing a leakage, installing brand-new flashing, or performing another kind of roofing repair work. Before you can begin your job, you have some huge questions to respond to: How will I spend for a brand-new roofing system or roofing system repair project?How can I choose a roof loan or other financing option that doesn't mess up my financial plan?There are financing options readily available for your roof task, however that does not mean each is the right suitable for you. However, if you resemble lots of individuals who need a roofing repair work or replacement, you probably can't relax and wait to save. A dripping or otherwise harmed roofing system suggests you require to find roofing financing rapidly. Your insurance coverage might cover your roofing system's damage if it was triggered by something beyond your controlsay a storm or fire. On the other hand, your insurance most likely will not cover any issues related to a lack of upkeep or natural wear and tear. You ought to check your policy or call your insurance business to discover any exemptions, coverage restrictions, etc. Coverage from property owners insurance coverage does not necessarily imply you will not need financing if you don't have cash. In the next two sections, we'll show you how you can finance your roof job. Roofing loans have a crucial advantage: you get the cash you require upfront. Although this lack of versatility might seem cumbersome, it really incentivizes you to map out a detailed budget plan before you start. Houzz discovered that couple of house owners remain on spending plan throughout restorations, which causes overspending. Prior to getting the loan, you need to know how much financing you'll need for your roof replacement. We suggest speaking with 3 or more experts to get a robust price quote. The ideal roofing system replacement loan option for you depends on two elements: If you do not have nashvillepost.com/business/finance/article/21143258/franklin-firm-launches-insurance-company much equity in your house, then you'll have to consider an unsecured alternative such as a personal roof loan.

If you don't currently have a line of credit open with your bank, then it might take 4-6 weeks to apply for and receive funds for your brand-new roofing system. This timeframe is too long for numerous immediate roofing projects. Our Property owner's Guide to House Enhancement Loans, written in assessment with numerous individual finance professionals, will teach you more about finding the best loan for your roof replacement. Let's take a look at each loan alternative and see how your house equity and timeframe need to influence your decision: We described above how Hearth can assist you discover the https://goldenfs.org/the-wesley-group/ right individual loan for your roof. These loans will have lower rates than personal loans, however they can take 4-6 weeks to approve. You're likewise likely to pay substantial closing expenses, and could face prepayment penalties if you pay the loan back early. Like personal loans, home equity loans are likewise good for funding a roof replacement or major repair work. Your state and the federal government may have unique programs for some kinds of roofing system repair work. You might also be able to receive a roofing repair work grant. You can read our guide on FHA 203( k) enhance loans and our guide on home repair work loans for more information about these alternatives. The Definitive Guide for Which Of These Best Fits The Definition Of Interest, As It Applies To Finance?

You prevent the pitfall of paying interest and fees on more cash than you eventually use. You have 2 main roofing funding choices in this category: charge card and house equity credit lines. Let's take a look at each. Under the best scenarios, a charge card can be an excellent alternative for a roofing task. Charge card let you obtain cash up to a pre-defined credit line, and if you repay your balance quickly, you may have the ability to prevent debt that quickly grows out of control. In this area, we'll go over the types of cards we provide, inform you when to consider a charge card, and go over when you must look somewhere else. These cards have no interest for an initial period, typically 6 to 18 months. You could finance your new roof without paying any interest if you pay down your balance prior to this initial duration ends. Check out 0% house improvement charge card through Hearth. If your credit requires work, you most likely want to save cash or put in the time to repair your credit report prior to considering a brand-new roofing system job. However sometimes you can't wait. If you have an emergency leak or other issue, then a charge card might be your only option. Make certain to develop a plan to pay down the card as rapidly as possible because interest can rapidly grow. You can use a charge card to finance any roofing task from repairing a couple of damaged shingles, to fixing flashing around your chimney, to installing a brand-new mobile house roof. If you are confident you can repay the card rapidly, then a card might be a great fit. Otherwise, you might wish to conserve cash unless you just can't wait. Like a credit card, you can borrow from a house equity credit line as required up to a predefined limit. Nevertheless, unlike a charge card, your bank uses your house equity as collateral for your loan. In return for using you lower rates than you 'd find somewhere else, your bank can take your home if you default on the loan. Roofing specialists may use funding to help you afford your project. Some companies, such as Stay Dry Roof, utilize financing services like Hearth that let consumers compare several options to find excellent rates. Other professionals may just give their customer a couple of https://receive.news/09/09/2020/wesley-financial-group-diversifies-with-the-launch-of-wesley-mutual/ financing options. If you're going to use your professional to find roof financing, make sure the business uses a funding partner that lets you compare throughout a number of choices so you can discover the finest rates. Here are five easy suggestions to follow for roofing remodelling success: Getting at least 3 quotes from specialists offers you an accurate image for your roof remodel cost. |

RSS Feed

RSS Feed