|

Because private money loans do not originate from standard lending institutions, they can be perfect for financiers looking for innovative funding. likewise understood as an owner carryback - is best for property that's owned free and clear. Buyer and seller can avoid the relatively endless paperwork of getting a mortgage and the seller might be able to carry out a 1031 exchange to defer paying capital gains tax - how old of a car can i finance for 60 months. When utilizing this alternative, be sure to keep an eye on your general debt-to-income ratio and the change in capital. are a fantastic method to raise capital for a greater deposit and increase the capital reserve account. Because there might be several customers in a JV, loan providers may be more relaxed in their loan terms and use better rate of interest in exchange for the reduced risk. Some investors choose to keep their equity intact, with a low loan balance and strong capital. Other rental homeowner turn accumulated equity into capital with cash-out refinancing, utilizing those funds to buy additional rentals and scale up the portfolio. Requirements for financial investment property cash-out refinancing vary from loan provider to lending institution. The 8-Minute Rule for How Many Years Can You Finance A Boat

Keep in mind that from the lender's viewpoint, that's the very same thing as getting a 25% deposit on the brand-new mortgage. If you have actually owned existing rental home over the past couple of years, the chances are you have actually built up a substantial amount of equity from rising market price. As an example, let's state you acquired a single-family rental home 5 years ago with a $100,000 loan amount. Your cash-out refinancing would yield: $150,000 present worth x 75% new mortgage = $112,500 - $80,000 existing loan balance benefit = $32,500 in available capital for additional realty investments. Initially glance, financing numerous rental residential or commercial properties might appear like a difficult dream. But with a little creativity and advanced preparation, it's simple to make that dream come to life. Aim for an individual credit report of at least 720 to increase your ability to get approved for more than one mortgage and to acquire the most favorable rates of interest and loan terms possible. Be a credible customer by having individual information and monetary efficiency reports of your current rental property prepared ahead of time. All About What Does A Finance Major Do

Look around for a lending institution the very same way you would go shopping around for a financial investment residential or commercial property, and offer to bring your loan provider repeat business and referrals as you continue to grow your rental home portfolio. For many years, you've been vigilantly settling your individual debt. You have actually finally got a healthy cost savings account. You're moneying your 401(k). Whatever is working out, however something is still missing out on: You 'd truly like to provide genuine estate investing a shot. The most significant barrier that's tripping you up is the financing procedure. There are always a few wrinkles to be ironed out. But if you're considering the purchase of residential or commercial property, sort through your different choices and be sure to consist of the following. Plenty of investors continue to use regional banks and cooperative credit union to finance realty financial investments, but those are no longer the only choices. How Old Of An Rv Can You Finance for Dummies

Instead, the honor of many hassle-free lending option has gone to online loan markets like LendingTree, LoanDepot, Quicken Loans, and Rocket Home mortgage. With an online loan market, you do not need to lose time driving from one bank to another and sitting in on lots of dull meetings, just to hear the very same old spiel again. Are you having difficulty receiving a mortgage? Or possibly the rates of interest you're used simply isn't possible offered your numbers? One option is to hold off for a few more months and store more cash. If you can put 25 percent down or more, you can conserve significantly on the interest. Seller funding is a smart option that frequently works when a financier can't get a loan from a bank or other standard loaning source. In this case, the seller of the propertywhich is usually owned free and clearessentially ends up being the bank. You take ownership of the home, but then cut monthly "home mortgage" payments to the previous owner. Not known Facts About How Long Can You Finance A Camper

If you attempt to pursue seller funding, you need to get together a clever tactical plan. Approaching a seller with no information isn't going to influence his/her confidence. You need to have actually particular terms written out and ready to be carried out. There's something to be stated for owning a piece of realty free and clear. You probably aren't in a position where you're able to buy a property with money on your own certainly. But thankfully, you do not need to. You have the choice to gather a group of financiers and enter together. Let's state you have an interest in buying a $200,000 rental home, for example. This is a terrific way to get your feet damp while spreading out the risk. You never want to rush into purchasing a residential or commercial property. It does not matter whether it's going to be your personal residence or a leasing. Nothing good ever takes place in genuine estate investing when the trigger is pulled prematurely.

0 Comments

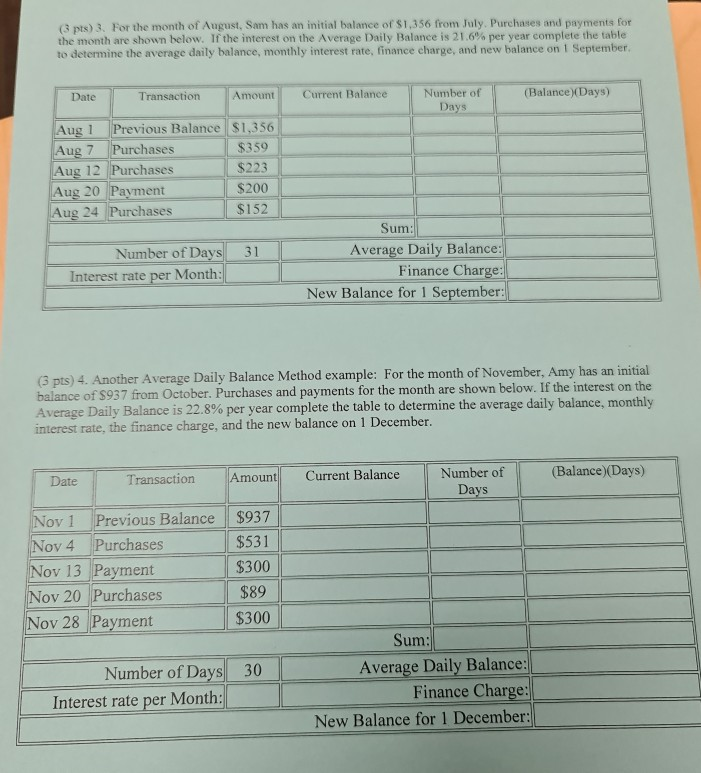

Interest rates can differ based upon the kind of loan item. Since a protected loan is backed by some sort of property or collateral, it is perceived to have less threat and feature a lower interest rate (APR) than an unsecured loan might use. An unsecured loan, such as a credit card, is extended solely on the credit history of the debtor and generally carries a higher APR due to the fact that the lender need to presume more threat if they aren't repaid. The calculation of finance charges differs depending on the sort of financial obligation included. For charge card financial obligation, finance charges are based on the average day-to-day balance on the credit card over the financing duration, which determines interest by taking the balance owed at the end of each day into account. If the interest compounds monthly, then a loan provider's financing charge formula for the typical daily balance will look like this: Average Daily Balance = (A/ D) x (I/ P) Where: A = the total everyday balances in the billing period, D = the number of days in the billing period, I = yearly portion rate, P = number of billing periods each year (usually 12) If the interest substances daily, however, the lending institution will calculate the financing charge by computing each day's ending balance and include this interest to the next day's start balance. (Note: The ending day-to-day balance considers the day's charges, payments, deposits, and withdrawals whether the lender uses day-to-day interest intensifying or regular monthly interest compounding.) Let's look at an example. The tables below compare how the interest would intensify monthly (left table) and how the interest would compound day-to-day (ideal table). You can see on the bottom of the left table how regular monthly compounding creates interest more slowly than daily interest compounding does. In this case, the borrower's charge card balance would produce $12. 55 in interest finance charges if the interest compounded month-to-month versus $12. 60 in interest finance charges if the interest intensified daily. And as you may think of, the bigger the charge card balance, the faster the interest charges speed up, especially with credit cards that use daily interest compounding (What does leverage mean in finance). Under the Truth in Lending Act, lending institutions are needed to plainly reveal all interest rates, basic charges, and penalty costs associated with the loan item to the debtor. In 2009, The Credit Card Responsibility, Responsibility and Disclosure Act (CARD) mandated a 21-day grace duration from brand-new finance and interest charges after a purchase is used a charge card. Other laws at the federal, state, and regional levels likewise fight predatory financing practices (Trade credit may be used to finance a major part of a firm's working capital when). In United States law, a finance charge is any cost representing the cost of credit, http://emilioxrqo723.yousher.com/all-about-what-does-principal-mean-in-finance or the cost of loaning. It is interest accrued on, and costs charged for, some forms of credit. It includes not only interest but other charges too, such as monetary deal fees. Information regarding the federal meaning of financing charge are found in the Truth-in-Lending Act and Guideline Z, promoted by the Federal Reserve Board. In personal financing, a finance charge may be considered merely the dollar quantity paid to borrow money, while interest is a portion quantity paid such as interest rate (APR).

The Basic Principles Of What Does Ria Stand For In Finance

Lenders and lenders use various approaches to determine finance charges. The most typical formula is based upon the typical daily balance, in which daily outstanding balances are included together and then divided by the number of days in the month. In financial accounting, interest is specified as any charge or expense of borrowing cash. Interest is a synonym for finance charge. In effect, the accounting professional takes a look at the whole cost of settlement on a Real Estate and Urban Advancement (HUD) kind 1 (the HUD-1 Settlement Statement) file as interest unless that charge can be recognized as an escrow quantity or a quantity that is credited present expenses or expenditures besides interest, such as payment of existing or prorated genuine estate taxes. ( 2003 ). Economics: Principles in Action. Upper Saddle River, New Jersey 07458: Pearson Prentice Hall. p. 513. ISBN 0-13-063085-3. CS1 maint: area (link) Kapoor, Jack R.; Dlabay, Les R.; Hughes, Robert J. (2007 ). Concentrate On Personal Financing. Mcgraw-Hill/Irwin Series in Finance, Insurance and Property (second ed.). Mcgraw-Hill. ISBN 0-07-353063-8. Giovetti, Al (2008 ). Accredited Organization Accounting Professional Review Course. Accreditation Council on Accounting and Taxation. A finance charge is the amount of the loan that is credited the debtor. It includes interest accrued and financial transaction fees. How many years can you finance a boat. Not quite the exact same as a rates of interest, the APR might confuse individuals who are looking for a car loan. How does APR work? Utilize these descriptions to assist build your monetary knowledge. Loans normally have numerous information and financing terms to examine. Take the rate of interest on a vehicle loan and the annual percentage rate (APR). Some Helpful hints people assume they refer to the same thing, however they do not. In fact, the APR is a much better gauge of what a loan will cost than the rates of interest alone. Dive into the information before you head to the automobile lot. If the rate of interest and the APR on a loan are different, the APR is normally greater. When it concerns APR vs. rate of interest, the APR really considers the total finance charge you pay on your loan, including prepaid financing charges such as loan charges and the interest that builds up prior to your first loan payment. When shopping for a loan, make sure you're comparing each lender's APR along with the rates of interest. In some cases dealerships run promotions that use buyers the option between a really low APR and a money rebate. It's not constantly instantly clear, nevertheless, which option provides the better deal. Even with an identical APR, you'll wind up paying more in interest throughout a longer term loan. Getting My How To Finance Building A House To Work

You're responsible for paying everything that's consisted of in the APR, even if your vehicle is totaled in a mishap or stolen car insurance might not constantly cover the total you owe. SPACE (Guaranteed Possession Security) insurance coverage may provide you with monetary defense if your vehicle is ever totaled or stolen and the insurance coverage settlement amount does not cover the unsettled primary balance due on your loan. That could suggest you won't need to roll the unpaid primary balance of the existing loan into the cost of funding a brand-new automobile. Buy your loan before you purchase your automobile to identify readily available rates of interest, APRs Click to find out more and repayment durations. Amortization Amortization explains the procedure of gradually paying off your car loan. In an amortizing loan, for each of your regular monthly payments, a portion is used towards the amount of the loan the principal and a portion of the payment is used towards paying the finance charge the interest. Interest Rate (APR) The Annual Percentage Rate (APR) is the expense you pay each year to obtain cash, consisting of costs, revealed as a percentage. The APR is a more comprehensive procedure of the expense to you of obtaining cash considering that it shows not only the interest rate however also the charges that you need to pay to get the loan. If you have 20% down, our company believe you deserve your home of choice no matter what your credit report is!Our network of real estate investors comprehend that great house buyers often have extremely few choices to purchase a home, for that reason they are delighted to facilitate a transaction with owner financing as a method to bridge a deal (How to finance an engagement ring). There are no prepayment charges so a future property owner can resolve their financing difficulties and re-finance the residential or commercial property into their own name anytime. As our experts about more details anytime to see if this program is the best suitable for you.

Owner financing is a monetary arrangement in between the seller and buyer of a house. Rather of dealing with a lending institution to get a home loan, the buyer makes monthly payments to the seller. If you're a get out of bluegreen timeshare real estate investor seeking to purchase your next property for your service, owner financing might have the ability to provide you chances you can't get with standard mortgage lenders. Before you start trying to find sellers who want to provide such an arrangement, however, comprehend how the procedure of owner funding works and both the advantages and disadvantages to consider. Owner financing permits homebuyersmostly real estate investors, however anyone can utilize itto purchase a home and pay the seller straight instead of getting a home loan. For example, if your credit history is reasonably low, you're self-employed or you're having a difficult time confirming your earnings, owner financing might be an option where conventional home mortgage lenders won't work with you. For the owner, the main advantage is getting a stable stream of income (with interest attached) till the property is paid for completely. Depending on where you live, owner funding can pass many names, consisting of: Owner funding Seller financing Owner brought funding Owner carryback Owner will bring (OWC) All of these terms essentially suggest the same thing, but we'll use "owner funding" and "seller funding" for the sake of simplicity. How to owner finance a home. Submit a single application online You can find out more and Find out more In general, the terms with a seller financing arrangement will look rather various than what you might discover with a conventional loan or bank financing. This is mainly due to the fact that unlike a lender, which owns hundreds and even countless home loan, a seller may only have one owner financing arrangement. This gives sellers a little more versatility, however it can also posture a higher threat. Here's a summary of what to anticipate with owner financing terms. A house seller doesn't have any minimum deposit requirements set by a bank or government company. Lease Or Finance A Car Which Is Better Can Be Fun For Anyone

Sometimes, you may be able to find an owner funding arrangement with a low deposit. But you're more likely to see higher down payment requirements, some as high as 25% or more. That's since the down payment amount is what you stand to lose if you default on the loan. The higher your down payment, the more "skin in the video game" you have, and you're less most likely to stop paying. Whatever the seller requests for, nevertheless, it might be negotiable. So if you don't have the quantity of money the seller desires or you do however want to maintain an emergency situation fund, ask if there's any wiggle space. In some circumstances, you may see rates of interest as high as 10% (or more), depending on your credit reliability, down payment and the general structure of the offer. In others, rates of interest may be lower. A 30-year mortgage is pretty typical for a basic home mortgage loan, though you might select to decrease to 15 years rather. With a seller funding arrangement, you might be able to pick a 30-year repayment, however the term will most likely be much shorter than that. For instance, the loan might amortize over 15 or 20 years, due to the fact that the owner does not wish to drag out the procedure over 3 years. Every owner financing arrangement is different, but to offer you a concept of how it might be structured, here's an example of a loan with a 30-year payment term and a balloon payment after 10 years. $200,000 $30,000 $170,000 8% 30 years 10 years $1,247. 40 $149,131. 96 $328,819. 96 Now, let's state you can negotiate with the owner of the house and exchange a higher deposit for a lower rate of interest and a balloon payment at 15 years. Here's how that may look. $200,000 $50,000 $150,000 6. 5% thirty years 15 years $948. 10 $108,839. 24 $329,497. 24 In the 2nd situation, you would save money on the loan's monthly payment. There are plenty of advantages of owner funding for both the seller and the buyer. Anybody who has actually gotten a home mortgage through a bank or banks understands it can be an inconvenience. A home mortgage loan begetter will request for substantial documents. Seller financing can be an easier procedure. Depending upon which side of the offer you're on, here's what you require to know. Faster closing time: Since it's just you and the seller exercising the offer, you do not require to await the loan underwriter, officer and bank's legal department to process and approve your loan. Less pricey to close: You don't need to stress about standard loan provider charges or a great deal of other expenses related to closing on traditional funding. What Does Alpha Mean In Finance Can Be Fun For Everyone

That's not to say you won't have any out-of-pocket costs, but they'll likely be much cheaper. Flexible credit requirements: If your credit is less than excellent, however your cash flow and reserves look good, you may have a much easier time getting authorized for a seller funding arrangement than a mortgage from a traditional loaning institution. Flexible down payment: While some sellers may require higher deposits, some might use to take less than what a bank might require for the very same funding offer (How to finance an engagement ring). 1-800Accountant is ideal for small companies. Our dedicated group of experienced accounting specialists and Discover more Can sell "as is": With a normal mortgage, the lending institution may have certain requirements of the collateral (the property) to safeguard its interests. With a seller funding agreement, there is no bank to please, and you may be able wfg presentation to offer the home as-is, conserving you a long time and money. (The buyer, in turn might use creative financing such as business credit cards to fix and turn the property.) Potentially good investment: Depending on the rate of interest you charge, you may be able to get a much better return on an owner funding arrangement than if you were to offer the house for a lump-sum payment and invest the cash elsewhere. And unlike the stock exchange, you do not have to fret about the return altering based on market conditions the rates of interest is set for the life of the loan (if that's how you structure the funding terms). Before you believe about anything else, you'll wish to find out where you're going to install your mobile home. The location you pick will have a big influence on the remainder of the process." Acquiring a mobile house and finding the right area is simply like purchasing a house," says Sexton - What does ach stand for in finance. "An excellent neighborhood is crucial." One option is to install the house on a piece of land that you currently own. You may also opt to buy the land where your mobile house will lie. Just ensure that zoning guidelines permit the installation of mobile homes on the lot that you own or want to purchase. Another option you can think about is renting a plot of land in a mobile house community. This needs less money upfront however includes a regular monthly lot rent costs to your housing expenses. Consult the manager of the neighborhood for restrictions on house functions and size and to find offered plots. Mobile homes and made homes come in a range of sizes, so you'll need to choose beforehand how large you desire your mobile home to be. Bigger houses are more expensive and require larger lots. As an outcome, you'll probably need to borrow more if you want a bigger home. You may see the terms single-wide and double-wide used. Single-wide homes are somewhat under 15 feet large, and double-wide houses are double that width. Both are typically about 70 feet long." Numerous towns don't allow single large mobile homes in their towns or city limits," says Sexton. "Ensure you investigate the rules that might use to your situation." Unlike standard real estate, mobile and manufactured houses tend to lose value over time. That implies you can get a discount if you buy a used mobile home. The compromise is that utilized mobile homes will often have indications of age unless they have actually been maintained effectively.

Some places will not allow the positioning of houses that were produced prior to a specific date, which limits your alternatives. timeshare salesperson With an older mobile home purchase, you will likely likewise need to utilize someone with knowledge and examination skills to ensure that you purchase a great home. Which results are more likely for someone without personal finance skills? Check all that apply.. Answer a few concerns to see which individual loans you pre-qualify for. The process fasts and easy, and it will not impact your credit rating. Mobile and produced homes can be a far more budget friendly choice than a conventional home. However if you plan to purchase one, do your research to find out what financing alternatives are available and understand the requirements to be qualified for the financing. The greater your credit rating, the simpler it will be to get approved for a mobile house loan with competitive interest rates." FHA will fund with a 500 to 589 credit report and 10 percent down," states Sexton. "Credit history with 580 or above will only be needed to have a deposit of 3. 5 percent. The minimum credit rating with Freddie Mac or Fannie Mae is 620 - How old of a car will a bank finance. Different Chattel loan service providers will require a credit report of just 575 credit rating or as high as a 660." The length of financing for your mobile home depends on the lending institution you utilize. Some Ideas on What Is The Lowest Credit Score Nissan Will Finance You Should Know

Due to the fact that mobile homes diminish in value gradually, it can be harder to find a lending institution that offers produced house financing than if you were buying a traditional home. That said, there are still a lot of alternatives readily available. Just make certain to do your due diligence to discover the right one for you based on your credit reliability, your monetary situation and your requirements and preferences. A mobile house loan is a loan for factory-built homes that can be put on a piece of land. Designs may differ from modest trailers to homes that look like houses connected completely to the land upon which they sit. Mobile house loans vary from a conventional residential or commercial property loan because the majority of loan providers and counties do not consider them real residential or commercial property, but rather individual home. In truth, in lots of counties, a mobile home is taxed by the department of motor automobiles rather than the home tax assessor. In many cases, if you wish to purchase a mobile house and location it on land that you rent, your loan will more carefully resemble an individual loan, with higher rates of interest and much shorter terms than a standard home mortgage. Some house lending institutions do have loans for mobile homes if they are Website link attached to the property owner's land. Others, and there are fewer of them, will lend on a mobile house even if it sits on land you lease. The loan providers we've evaluated have loan amount ranges from $75,000 to $2 million for jumbo loan programs. The debt-to-income (DTI) ratio ceiling for the majority of loan providers remains in the low 40s. The lender will utilize your DTI and income to identify just how much you can borrow. If you receive among the government-backed loan programs, such as the FHA, VA, or USDA, you can buy a mobile house with a 3. If you own the land or plan to purchase the land together with the mobile house, you'll have more loan provider alternatives than if you wish to purchase a mobile house that beings in a leased lot in a mobile house park (What is a consumer finance account). When you buy a mobile home, it is not required to own the land, but it will open up more loan alternatives for you. Mobile homes are in some cases located in a mobile house park where the park owner holds title to the land and you rent it. In these cases, the property owner rents a plot of land but owns the mobile house itself.

Additionally, owners of mobile homes can position mobile homes on land they own or land they are buying in conjunction with the mobile house. When you own the land and the home, your loan rates and terms will be much better, and you'll have more providing alternatives. The lending institutions we've reviewed and picked as the best can work with low credit scores in the 500 and 600 range. A credit report lower than 500 might not qualify at all. Naturally, higher credit report will always get you much better rates and terms. Credit rating in the 700s and 800s will get the most affordable rate of interest. The Buzz on Which Of These Best Fits The Definition Of Interest, As It Applies To Finance?

Standard loans will not be so forgiving of ratings listed below 700. You might get your loan authorized, but it will bring greater rates and a regard to twenty years or less. We examined 12 mobile home loan providers to choose the very best 5. We analyzed business history and track record, whether they funded both newly constructed and used mobile homes, and their minimum and optimum loan worth limits. Customer qualifications mattered, too. We compared companies to see who permitted debtors to have lower credit ratings, higher debt-to-income ratios, and whether they had low-down-payment programs. Lastly, we examined loan provider requirements for whether you Additional resources rented or owned the land upon which your mobile home would sit. A swap, in financing, is a contract between two counterparties to exchange financial instruments or cashflows or payments for a particular time. The instruments can be almost anything but many swaps involve money based upon a notional principal quantity. The general swap can likewise be viewed as a series of forward contracts through which two celebrations exchange monetary instruments, resulting in a common series of exchange dates and 2 streams of instruments, the legs of the swap. The legs can be nearly anything however typically one leg involves capital based on a notional principal quantity that both parties consent to. In practice one leg is usually repaired while the other varies, that is determined by an uncertain variable such as a benchmark rates of interest, a foreign exchange rate, an index price, or a product price. Swaps are mostly over the counter agreements in between business or monetary institutions (What is internal rate of return in finance). Retail financiers do not generally take part in swaps. A home mortgage holder is paying a floating rate of interest on their home mortgage however expects this rate to increase in the future. Another home mortgage holder is paying a fixed rate however expects rates to fall in the future. They get in a fixed-for-floating swap arrangement. Both home mortgage holders agree on a notional principal quantity and maturity date and accept handle each other's payment responsibilities. By using a swap, both celebrations efficiently altered their home mortgage terms to their favored interest mode while neither party needed to renegotiate terms with their home mortgage loan providers. Thinking about the next payment just, both celebrations might as well have actually gotten in a fixed-for-floating forward agreement. For the payment after that another forward agreement whose terms are the same, i. e. same notional amount and fixed-for-floating, and so on. The swap contract for that reason, can be viewed as a series of forward agreements. In the end there are two streams of cash streams, one from the celebration who is always paying a fixed interest on the notional quantity, the fixed leg of the swap, the other from the celebration who accepted pay the drifting rate, the drifting leg. Swaps were first introduced to the general public in 1981 when IBM and the World Bank participated in a swap agreement. Today, swaps are amongst the most greatly traded financial contracts worldwide: the total amount of rates of interest and currency swaps outstanding was more than $348 trillion in 2010, according to Bank for International Settlements (BIS). The majority of swaps are traded over the counter( finance timeshare OTC), "tailor-made" for the counterparties. The Dodd-Frank Act in 2010, nevertheless, envisions a multilateral platform for swap pricing estimate, the swaps execution facility (SEF), and mandates that swaps be reported to and cleared through exchanges or clearing homes which consequently caused the development of swap data repositories (SDRs), a main facility for swap data reporting and recordkeeping. futures market, and the Chicago Board Options Exchange, signed up to end up being SDRs. They began to list some types of swaps, swaptions and swap futures on their platforms. Other exchanges followed, such as the Intercontinental, Exchange and Frankfurt-based Eurex AG. According to the 2018 SEF Market Share Statistics Bloomberg dominates the credit rate market with 80% share, TP dominates the FX dealership to dealership market (46% share), Reuters controls the FX dealership to client market (50% share), Tradeweb is strongest in the vanilla rate of interest market (38% share), TP the greatest platform in the basis swap market (53% share), BGC dominates both the swaption and XCS markets, Custom is the most significant platform for Caps and Floors (55% share). At the end of 2006, this was USD 415. 2 trillion, more than 8. 5 times the 2006 gross world product. However, because the capital generated by a swap is equal to a rate of interest times that notional quantity, the cash circulation created from swaps is a substantial portion of but much less than the gross world productwhich is likewise a cash-flow procedure. Most of this (USD 292. 0 trillion) was due to rate of interest swaps. These divided by currency as: Source: BIS Semiannual OTC derivatives stats at end-December 2019 Currency Notional outstanding (in USD trillion) End 2000 End 2001 End 2002 End 2003 End 2004 End http://anationofmoms.com/2020/04/real-estate-terms-tips.html 2005 End 2006 16. 9 31. 5 44. 7 59. 3 81. 4 112. 1 13. 0 18. 9 23. 7 33. 4 44. 8 74. 4 97. 6 11. 1 10. 1 12. 8 17. 4 21. 5 25. 6 38. 0 4. 0 5. 0 6. 2 7. 9 11. 6 15. 1 22. 3 1. 1 1. 2 1. 5 2. 0 2. 7 3. 3 3. 5 Source: "The International OTC Derivatives Market at end-December 2004", BIS, , "OTC Derivatives Market Activity in the Second Half of 2006", BIS, A Major Swap Participant (MSP, or in some cases Swap Bank) is a generic term to describe a banks that helps with swaps between counterparties. Not known Details About Trade Credit May Be Used To Finance A Major Part Of A Firm's Working Capital When

A swap bank can be a worldwide commercial bank, a financial investment bank, a merchant bank, or an independent operator. A swap bank works as either a swap broker or swap dealer. As a broker, the swap bank matches counterparties but does not assume any danger of the swap. The swap broker receives a commission for this service. Today, the majority of swap banks serve as dealerships or market makers. As a market maker, a swap bank is prepared to accept either side of a currency swap, and after that later on-sell it, or match it with a counterparty. In this capacity, the swap bank presumes a position in the swap and therefore assumes some threats. The 2 main reasons for a counterparty to utilize a currency swap are to get debt financing in the switched currency at an interest cost reduction brought about through comparative advantages each counterparty has in its national capital market, and/or the benefit of hedging long-run exchange rate direct exposure. These reasons appear uncomplicated and tough to argue with, especially to the degree that name acknowledgment is truly crucial in raising funds in the worldwide bond market. Companies utilizing currency swaps have statistically higher levels of long-lasting foreign-denominated debt than companies that utilize no currency derivatives. Alternatively, the primary users of currency swaps are non-financial, global companies with long-lasting foreign-currency funding requirements. Funding foreign-currency financial obligation utilizing domestic currency and a currency swap is for that reason exceptional to financing directly with foreign-currency financial obligation. The 2 primary factors for swapping rate of interest are to better match maturities of possessions and liabilities and/or to acquire an expense savings through the quality spread differential (QSD). Empirical proof recommends that the spread between AAA-rated commercial paper (floating) and A-rated commercial is somewhat less than the spread between AAA-rated five-year obligation (fixed) and an A-rated obligation of the very same tenor. These findings suggest that companies with lower (greater) credit rankings are more likely to pay repaired (drifting) in swaps, and fixed-rate payers would utilize more short-term financial obligation and have shorter debt maturity than floating-rate payers. |

RSS Feed

RSS Feed