|

Can you subtract the interest on an individual loan used to buy or develop a tiny home, if you're utilizing it as a primary or secondary house? That concern appears to be up in the air. "As far as we can inform, the response is no," stated Kai Rostcheck, executive director of Tiny Home Loaning. While the Internal Revenue Service allows you to deduct the interest on a loan protected by a motor home or even a boat used as a secondary or primary residence, an individual loan utilized to buy or construct a tiny house isn't secured by the home itself. Which's the secret, according to Internal Revenue Service Topic 505 - the property should act as security on the loan in order for the interest to be tax-deductible. " Where we are remains in the very early days of small houses becoming legitimized," Rostcheck said. "It's been a fringe movement for a very long time - what is a beta in finance." Tax deductibility is one example of that. Tiny houses are still so new that loan providers are simply starting to find out how to classify them and develop standards for approving those loans. Other locations, such as zoning and building regulations, remain unclear also, Rostcheck stated. That not only makes it hard to qualify those homes for a loan, but affects where they can be situated as well, and the guidelines differ across the nation. "It resembles the Wild West, literally, it alters from town to town," Rostchek stated. Many won't allow houses on a structure or permanently sited manufactured houses of less than 800 square feet, while still others have no minimum size requirement for completely sited houses. Depending on whether the house will be mobile or completely sited, there might be different challenges with regard to connecting to utilities or otherwise supplying water, sewer and electrical service. The 8-Minute Rule for Which Of These Methods Has The Highest Finance Charge

Another obstacle to standard mortgage loaning for tiny homes is getting insurance. House owner's insurance coverage needs that a system be put on a structure, however the reality many tiny homes are on wheels develops some significant issues. "How do we give you what is basically a property owners' policy understanding it west land financial could be moved, meaning we 'd have to re-write the policy, and there could be liability issues when moving it?" Rostcheck asked.

" No having simple access to funding has been a huge throttle on the industry" Rostcheck said, but he's positive the market will eventually get it all worked out, offered the size of the prospective market. "We have a woeful absence of economical housing in this nation," Rostcheck stated. He notes that according to Census figures, a little over one-third of all families, or 45 million, are tenants, paying an average of $1,000 month, for a market total of $45 billion. Even if only 1 percent of renters were to ultimately buy small homes, he stated, that's still a quite big market. "I believe that's the most engaging reason banks are ultimately going to get on board with it" he stated. Lightstream's Nelson concurs. "I believe that Millennials are thinking extremely in a different way about own a home than the previous two generations," he stated. There might be interest from baby boomers aiming to downsize too. For the mobile alternative, Nelson stated a tiny house enables more personalization than a basic Recreational Vehicle and enables people to get a bit imaginative too. "You have actually got the flexibility to build something that actually fulfills your requirements," he stated. Program more You generally have a few alternatives when funding a small home: Numerous small houses are on wheels. If that's what you're trying to find, Recreational Vehicle loans might assist you with funding. To qualify, your home requires to be certified by the Recreational Car Market Association, that makes sure it meets security requirements for living and taking a trip on the road. An Unbiased View of How To Finance A House Flip

You can get this kind of funding either through your home's producer or a service provider that offers Recreational Vehicle loans. If you're aiming to buy a small house with a solid structure or wish to build your own RV, you might wish to consider securing an unsecured personal loan. You can usually use these term loans for any genuine function and do not have to put your house up as security - what is the meaning of finance. That way, you'll have continuous access to funds and can get what you need, when you need it. A personal line of credit can prepare you for unanticipated costs that don't factor into your preliminary calculations. While your small home likely won't be eligible for a standard home loan, you might still be able to get approved for a chattel mortgage. Effects home loans can be specifically helpful if you park your tiny house on leased land or plan on moving regularly. They tend to have lower interest rates than individual loans and might have lest stringent eligibility requirements than other financing alternatives. Non-traditional homes require unconventional forms of financing. A lot of home https://calenevhgy.doodlekit.com/blog/entry/21203166/how-long-can-you-finance-a-boat-for-truths loans feature minimum limits on how much you can borrow, which tiny houses frequently do not meet. Imagine this situation: Amelia just recently finished from college and was filled with student debt. Owning a home was constantly an imagine hers, but arriving seemed difficult with her month-to-month student loan payments and entry-level task. A small house, nevertheless appeared like a possibility which ended up being a truth when she found a pre-built are timeshare exit companies legit Recreational Vehicle house for $68,000 through a small home producer. She got a 15-year loan with a 5. 59% rate of interest and a 20% deposit of $13,535. 60 which her parents loaned her without interest. This implied that she had 15 years of regular monthly repayments of $445. Other expenses included a $97. 02 annual registration cost for a 9,000-pound trailer in New york city State and a $950 monthly rental charge for a Recreational Vehicle spot with electrical power and water included. Excitement About How To Get A Car On Finance

They tend to cost a portion of a routine house, which can come with thousands of square footage. However that doesn't mean it's cheap. How much you can expect to pay depends on whether you intend on purchasing a tiny home or developing one. It also depends upon your location's regulations. Others have limitations to camping on private land which applies to your home if it's classified as a Recreational Vehicle. Make sure you know your local laws before deciding where or what to build. This can be the most convenient way to do things, but there are still a number of expenses to think about, especially if it's a Recreational Vehicle. If you're buying a Recreational Vehicle, you can either buy land, park it on personal residential or commercial property belonging to good friends or household, lease a long-lasting RV spot or move it around public land. However you'll likewise spend for a trailer license, annual RV registration fees not to discuss having a cars and truck strong enough to drive it around - what is a finance charge on a car loan.

0 Comments

[D-MD] Brownley, Julia [D-CA] Buchanan, Vern [R-FL] Buck, Ken [R-CO] Bucshon, Larry [R-IN] Budd, Ted [R-NC] Burchett, Tim [R-TN] Citizen, Michael C. [R-TX] Bush, Cori [D-MO] Bustos, Cheri [D-IL] Butterfield, G. K. [D-NC] Calvert, Ken [R-CA] Cammack, Kat [R-FL] Carbajal, Salud O. [D-CA] Cardenas, Tony [D-CA] Carl, Jerry L. [R-AL] Carson, Andre [D-IN] Carter, Earl L. "Buddy" [R-GA] Carter, John R. [R-TX] Cartwright, Matt [D-PA] Case, Ed [D-HI] Casten, Sean [D-IL] Castor, Kathy [D-FL] Castro, Joaquin [D-TX] Cawthorn, Madison [R-NC] Chabot, Steve [R-OH] Cheney, Liz [R-WY] Chu, Judy [D-CA] Cicilline, David N. [D-RI] Clark, Katherine M. [D-MA] Clarke, Yvette D. [D-NY] Cleaver, Emanuel [D-MO] Cline, Ben [R-VA] Cloud, Michael [R-TX] Clyburn, James E. [D-SC] Clyde, Andrew S. [R-GA] Cohen, Steve [D-TN] Cole, Tom [R-OK] Comer, James [R-KY] Connolly, Gerald E. [D-VA] Cooper, Jim [D-TN] Correa, J. Luis [D-CA] Costa, Jim [D-CA] Courtney, Joe [D-CT] Craig, Angie [D-MN] Crawford, Eric A. [R-UT] Davids, Sharice [D-KS] Davidson, Warren [R-OH] Davis, Danny K. [D-IL] Davis, Rodney [R-IL] Dean, Madeleine [D-PA] De, Fazio, Peter A. [D-OR] De, Gette, Diana [D-CO] De, Lauro, Rosa L. [D-CT] Del, Bene, Suzan K. [D-WA] Delgado, Antonio [D-NY] Demings, Val Butler [D-FL] De, Saulnier, Mark [D-CA] Des, Jarlais, Scott [R-TN] Deutch, Theodore E. [D-FL] Diaz-Balart, Mario [R-FL] Dingell, Debbie [D-MI] Doggett, Lloyd [D-TX] Donalds, Byron [R-FL] Doyle, Michael F. [D-PA] Duncan, Jeff [R-SC] Dunn, Neal P. [R-FL] Emmer, Tom [R-MN] Escobar, Veronica [D-TX] Eshoo, Anna G. [D-CA] Espaillat, Adriano [D-NY] Estes, Ron [R-KS] Evans, Dwight [D-PA] Fallon, Pat [R-TX] Feenstra, Randy [R-IA] Ferguson, A. Drew, IV [R-GA] Fischbach, Michelle [R-MN] Fitzgerald, Scott [R-WI] Fitzpatrick, Brian K. [R-PA] Fleischmann, Charles J. "Chuck" [R-TN] Fletcher, Lizzie [D-TX] Fortenberry, Jeff [R-NE] Foster, Costs [D-IL] Foxx, Virginia [R-NC] Frankel, Lois [D-FL] Franklin, C.

[D-OH] Fulcher, Russ [R-ID] Gaetz, Matt donate timeshare to charity [R-FL] Gallagher, Mike [R-WI] Gallego, Ruben [D-AZ] Garamendi, John [D-CA] Garbarino, Andrew R. [R-NY] Garcia, Jesus G. "Chuy" [D-IL] Garcia, Mike [R-CA] Garcia, Sylvia R. [D-TX] Gibbs, Bob [R-OH] Gimenez, Carlos A. [R-FL] Gohmert, Louie [R-TX] Golden, Jared F. [D-ME] Gomez, Jimmy [D-CA] Gonzales, Tony [R-TX] Gonzalez, Anthony [R-OH] Gonzalez, Vicente [D-TX] Gonzalez-Colon, Jenniffer [R-PR] Great, Bob [R-VA] Gooden, Lance [R-TX] Gosar, Paul A. [R-AZ] Gottheimer, Josh [D-NJ] Granger, Kay [R-TX] Graves, Attic [R-LA] Graves, Sam [R-MO] Green, Al [D-TX] Green, Mark E - How long can you finance a used car. [R-TN] Greene, Marjorie Taylor [R-GA] Griffith, H. Morgan [R-VA] Grijalva, Raul M. [D-AZ] Grothman, Glenn [R-WI] Guest, Michael [R-MS] Guthrie, Brett [R-KY] Haaland, Debra A - The trend in campaign finance law over time has been toward which the following?. [D-NM] Hagedorn, Jim [R-MN] Harder, Josh [D-CA] Harris, Andy [R-MD] Harshbarger, Diana [R-TN] Hartzler, Vicky [R-MO] Hastings, Alcee L. [D-FL] Hayes, Jahana [D-CT] Hern, Kevin [R-OK] Herrell, Yvette [R-NM] Herrera Beutler, Jaime [R-WA] Hice, Jody B. French [R-AR] Himes, James A. [D-CT] Hinson, Ashley [R-IA] Hollingsworth, Trey [R-IN] Horsford, Steven [D-NV] Houlahan, Chrissy [D-PA] Hoyer, Steny H. [D-MD] Hudson, Richard [R-NC] Huffman, Jared [D-CA] Huizenga, Bill [R-MI] Issa, Darrell E. [R-CA] Jackson, Ronny [R-TX] Jackson Lee, Sheila [D-TX] cancel bluegreen timeshare Jacobs, Chris [R-NY] Jacobs, Sara [D-CA] Jayapal, Pramila [D-WA] Jeffries, Hakeem S (Which of the following approaches is most suitable for auditing the finance and investment cycle?). [D-NY] Johnson, Expense [R-OH] Johnson, Dusty [R-SD] Johnson, Eddie Bernice [D-TX] Johnson, Henry C. "Hank," Jr. [D-GA] Johnson, Mike [R-LA] Jones, Mondaire [D-NY] Jordan, Jim [R-OH] Joyce, David P. [R-OH] Joyce, John [R-PA] Kahele, Kaiali'i [D-HI] Kaptur, Marcy [D-OH] Katko, John [R-NY] Keating, William R. [D-MA] Keller, Fred [R-PA] Kelly, Mike [R-PA] Kelly, Robin L. [D-IL] Kelly, Trent [R-MS] Khanna, Ro [D-CA] Kildee, Daniel T. [D-MI] Kilmer, Derek [D-WA] Kim, Andy [D-NJ] Kim, Young [R-CA] Kind, Ron [D-WI] Kinzinger, Adam [R-IL] Kirkpatrick, Ann [D-AZ] Krishnamoorthi, Raja [D-IL] Kuster, Ann M. [D-RI] Larsen, Rick [D-WA] Larson, John B. [D-CT] Latta, Robert E. [R-OH] La, Turner, Jake [R-KS] Lawrence, Brenda L. [D-MI] Lawson, Al, Jr. [D-FL] Lee, Barbara [D-CA] Lee, Susie [D-NV] Leger Fernandez, Teresa [D-NM] Lesko, Debbie [R-AZ] Levin, Andy [D-MI] Levin, Mike [D-CA] Lieu, Ted [D-CA] Lofgren, Zoe [D-CA] Long, Billy [R-MO] Loudermilk, Barry [R-GA] Lowenthal, Alan S. [D-CA] Lucas, Frank D. [R-OK] Luetkemeyer, Blaine [R-MO] Luria, Elaine G. [D-VA] Lynch, Stephen F. [D-MA] Mace, Nancy [R-SC] Malinowski, Tom [D-NJ] Malliotakis, Nicole [R-NY] Maloney, Carolyn B. [D-NY] Maloney, Sean Patrick [D-NY] Mann, Tracey [R-KS] Manning, Kathy E. [D-NC] Massie, Thomas [R-KY] Mast, Brian J. [R-FL] Matsui, Doris O. [D-CA] Mc, Bath, Lucy [D-GA] Mc, Carthy, Kevin [R-CA] Mc, Caul, Michael T. [R-TX] Mc, Clain, Lisa C. [. R-MI] Mc, Clintock, Tom [R-CA] Mc, Collum, Betty [D-MN] Mc, Eachin, A. [D-MA] Mc, Henry, Patrick T. [R-NC] Mc, Kinley, David B. [R-WV] Mc, Morris Rodgers, Cathy [R-WA] Mc, Nerney, Jerry [D-CA] Meeks, Gregory W. [D-NY] Meijer, Peter [R-MI] Meng, Grace [D-NY] Meuser, Daniel [R-PA] Mfume, Kweisi [D-MD] Miller, Carol D. [R-WV] Miller, Mary E. [R-IL] Miller-Meeks, Mariannette [R-IA] Moolenaar, John R. [R-MI] Mooney, Alexander X. [R-WV] Moore, Barry [R-AL] Moore, Blake D. [R-UT] Moore, Gwen [D-WI] Morelle, Joseph D. [D-NY] Moulton, Seth [D-MA] Mrvan, Frank J. [D-IN] Mullin, Markwayne [R-OK] Murphy, Gregory [R-NC] Murphy, Stephanie N. [D-FL] Nadler, Jerrold [D-NY] Napolitano, Grace F. [D-CA] Neal, Richard E. [D-MA] Neguse, Joe [D-CO] Nehls, Troy E. [R-TX] Newhouse, Dan [R-WA] Newman, Marie [D-IL] Norcross, Donald [D-NJ] Norman, Ralph [R-SC] Norton, Eleanor Holmes [D-DC] Nunes, Devin [R-CA] O'Halleran, Tom [D-AZ] Obernolte, Jay [R-CA] Ocasio-Cortez, Alexandria [D-NY] Omar, Ilhan [D-MN] Owens, Burgess [R-UT] Palazzo, Steven M. [D-NJ] Palmer, Gary J. [R-AL] Panetta, Jimmy [D-CA] Pappas, Chris [D-NH] Pascrell, Bill, Jr. [D-NJ] Payne, Donald M., Jr. [D-NJ] Pelosi, Nancy [D-CA] Pence, Greg [R-IN] Perlmutter, Ed [D-CO] Perry, Scott [R-PA] Peters, Scott H. [D-CA] Pfluger, August [R-TX] Phillips, Dean [D-MN] Pingree, Chellie [D-ME] Plaskett, Stacey E. [D-VI] Pocan, Mark [D-WI] Porter, Katie [D-CA] Posey, Expense [R-FL] Pressley, Ayanna [D-MA] Price, David E. [D-NC] Quigley, Mike [D-IL] Radewagen, Aumua Amata Coleman [R-AS] Raskin, Jamie [D-MD] Reed, Tom [R-NY] Reschenthaler, Man [R-PA] Rice, Kathleen M. [D-NY] Rice, Tom [R-SC] Richmond, Cedric L. [D-LA] Rogers, Harold [R-KY] Rogers, Mike D. [R-AL] Rose, John W. [R-TN] Rosendale Sr., Matthew M. [R-MT] Ross, Deborah K. [D-NC] Rouzer, David [R-NC] Roy, Chip [R-TX] Roybal-Allard, Lucille [D-CA] Ruiz, Raul [D-CA] Ruppersberger, C. A (What is a swap in finance). Dutch [D-MD] Rush, Bobby L. The 8-Second Trick For How Did The Us Finance Ww1

[D-IL] Rutherford, John H. [R-FL] Ryan, Tim [D-OH] Sablan, Gregorio Kilili Camacho [D-MP] Salazar, Maria Elvira [R-FL] Sanchez, Linda T. Q. [D-GU] Sarbanes, John P. [D-MD] Scalise, Steve [R-LA] Scanlon, Mary Gay [D-PA] Schakowsky, Janice D. [D-IL] Schiff, Adam B. [D-CA] Schneider, Bradley Scott [D-IL] Schrader, Kurt [D-OR] Schrier, Kim [D-WA] Schweikert, David [R-AZ] Scott, Austin [R-GA] Scott, David [D-GA] Scott, Robert C. "Bobby" [D-VA] Sessions, Pete [R-TX] Sewell, Terri A. [D-AL] Sherman, Brad [D-CA] Sherrill, Mikie [D-NJ] Simpson, Michael K. [R-ID] Sires, Albio [D-NJ] Slotkin, Elissa [D-MI] Smith, Adam [D-WA] Smith, Adrian [R-NE] Smith, Christopher H. [R-NJ] Smith, Jason [R-MO] Smucker, Lloyd [R-PA] Soto, Darren [D-FL] Spanberger, Abigail Davis [D-VA] Spartz, Victoria [R-IN] Speier, Jackie [D-CA] Stanton, Greg [D-AZ] Stauber, Pete [R-MN] Steel, Michelle [R-CA] Stefanik, Elise M. [R-NY] Steil, Bryan [R-WI] Steube, W. Gregory [R-FL] Stevens, Haley M. [D-MI] Stewart, Chris [R-UT] Stivers, Steve [R-OH]. Strickland, Marilyn [D-WA] Suozzi, Thomas R. [D-NY] Swalwell, Eric [D-CA] Takano, Mark [D-CA] Taylor, Van [R-TX] Tenney, Claudia [R-NY] Thompson, Bennie G. [R-WI] Timmons, William R. IV [R-SC] Titus, Dina [D-NV] Tlaib, Rashida [D-MI] Tonko, Paul [D-NY] Torres, Norma J. [D-CA] Torres, Ritchie [D-NY] Trahan, Lori [D-MA] Trone, David J. [D-MD] Turner, Michael R. [R-OH] Underwood, Lauren [D-IL] Upton, Fred [R-MI] Valadao, David G. [R-CA] Van Drew, Jefferson [R-NJ] Van Duyne, Beth [R-TX] Vargas, Juan [D-CA] Veasey, Marc A. [D-TX] Vela, Filemon [D-TX] Velazquez, Nydia M. [D-NY] Wagner, Ann [R-MO] Walberg, Tim [R-MI] Walorski, Jackie [R-IN] Waltz, Michael [R-FL] Wasserman Schultz, Debbie [D-FL] Waters, Maxine [D-CA] Watson Coleman, Bonnie [D-NJ] Weber, Randy K., Sr. [R-TX] Webster, Daniel [R-FL] Welch, Peter [D-VT] Wenstrup, Brad R. [R-OH] Westerman, Bruce [R-AR] Wexton, Jennifer [D-VA] Wild, Susan [D-PA] Williams, Nikema [D-GA] Williams, Roger [R-TX] Wilson, Frederica S. [D-FL]. Wilson, Joe [R-SC] Wittman, Robert J. [R-VA] Womack, Steve [R-AR] Wright, Ron [R-TX] Yarmuth, John A. [D-KY] Young, Don [R-AK] Zeldin, Lee M. [D-CO] Blackburn, Marsha [R-TN] Blumenthal, Richard [D-CT] Blunt, Roy [R-MO] Booker, Cory A. [D-NJ] Boozman, John [R-AR] Braun, Mike [R-IN] Brown, Sherrod [D-OH] Burr, Richard [R-NC] Cantwell, Maria [D-WA] Capito, Shelley Moore [R-WV] Cardin, Benjamin L. [D-MD] Carper, Thomas R. [D-DE] Casey, Robert P., Jr. [D-PA] Cassidy, Bill [R-LA] Collins, Susan M. [R-ME] Coons, Christopher A. [D-DE] Cornyn, John [R-TX] Cortez Masto, Catherine [D-NV] Cotton, Tom [R-AR] Cramer, Kevin [R-ND] Crapo, Mike [R-ID] Cruz, Ted [R-TX] Daines, Steve [R-MT] Duckworth, Tammy [D-IL] Durbin, Richard J. [D-IL] Ernst, Joni [R-IA] Feinstein, Dianne [D-CA] Fischer, Deborah [R-NE] Gillibrand, Kirsten E. [D-NY] Graham, Lindsey [R-SC] Grassley, Chuck [R-IA] Hagerty, Bill [R-TN] Harris, Kamala D. [D-CA] Hassan, Margaret Wood [D-NH] Hawley, Josh [R-MO] Heinrich, Martin [D-NM] Hickenlooper, John W. [D-CO] Hirono, Mazie K. [D-HI] Hoeven, John [R-ND] Hyde-Smith, Cindy [R-MS] Inhofe, James M. [R-OK] Johnson, Ron [R-WI] Kaine, Tim [D-VA] Kelly, Mark [D-AZ] Kennedy, John [R-LA] King, Angus S., Jr. [D-VT] Lee, Mike [R-UT] Loeffler, Kelly [R-GA] Lujan, Ben Ray [D-NM] Lummis, Cynthia M. [R-WY] Manchin, Joe, III [D-WV] Markey, Edward J. [D-MA] Marshall, Roger W. [R-KS] Mc, Connell, Mitch [R-KY] Menendez, Robert [D-NJ] Merkley, Jeff [D-OR] Moran, Jerry [R-KS] Murkowski, Lisa [R-AK] Murphy, Christopher [D-CT] Murray, Patty [D-WA] Ossoff, Jon [D-GA] Padilla, Alex [D-CA] Paul, Rand [R-KY] Peters, Gary C. [D-MI] Portman, Rob [R-OH] Reed, Jack [D-RI] Risch, James E. [R-ID] Romney, Mitt [R-UT] Rosen, Jacky [D-NV] Rounds, Mike [R-SD] Rubio, Marco [R-FL] Sanders, Bernard [I-VT] Sasse, Ben [R-NE] Schatz, Brian [D-HI] Schumer, Charles E. [D-NY] Scott, Rick [R-FL] Scott, Tim [R-SC] Shaheen, Jeanne https://andersonwoiu156.edublogs.org/2022/05/27/facts-about-what-is-internal-rate-of-return-in-finance-revealed/ [D-NH] Shelby, Richard C. [R-AL] Sinema, Kyrsten [D-AZ] Smith, Tina [D-MN] Stabenow, Debbie [D-MI] Sullivan, Dan [R-AK] Tester, Jon [. D-MT]. Thune, John [R-SD] Tillis, Thom [R-NC] Toomey, Pat [R-PA] Tuberville, Tommy [R-AL] Van Hollen, Chris [D-MD] Warner, Mark R. economy.:3132 The NYSE and NASDAQ are the two biggest stock market in the world. New york city likewise leads in hedge fund management; private equity; and the financial volume of mergers and acquisitions. Several financial investment banks and financial investment managers headquartered in New York City are essential individuals in other monetary centres.:3435 The New York City Federal Reserve Bank, the largest within the Federal Reserve System, controls banks and implements U.S. monetary policy, which in turn influences the world's economy. The 3 significant international credit ranking companies Requirement and Poor's, Moody's Investor Service, and Fitch Scores are headquartered or coheadquartered in New york city City, with Fitch being coheadquartered in London. London has actually been a prominent global monetary centre because the 19th century, serving as a centre of financing and investment around the world.:7475:149 English contract law was adopted extensively for worldwide finance, with legal services offered in London. Banks situated there supplied services internationally such as Lloyd's of London (established 1686) for insurance coverage and the Baltic Exchange (founded 1744) for shipping. Throughout the 20th century London played an essential function in the development of new financial products such as the Eurodollar and Eurobonds in the 1960s, international possession management and worldwide equities trading in the 1980s, and derivatives in the 1990s.:13:6,1213,889 London continues to preserve a leading position as a monetary centre in the 21st century, and maintains the largest trade surplus in monetary services around the world. London is the largest centre for derivatives markets, foreign exchange markets, cash markets, issuance of global financial obligation securities, global insurance coverage, trading in gold, silver and base metals through the London bullion market and London Metal Exchange, and worldwide bank financing.:2 London take advantage of its position between the Asia and U.S. time zones, and took advantage of its location within the European Union,:1 although this ended on 31 January 2020 when the United Kingdom left the European Union following the Brexit referendum of 2016. As well as the London Stock Exchange, the Bank of England, the second earliest main bank, is in London, although the European Banking Authority relocated to Paris after Brexit. About What Does Ear Stand For In Finance

One report recommends that Japanese authorities are working on plans to transform Tokyo but have actually satisfied with blended success, noting that "preliminary drafts suggest that Japan's economic specialists are having difficulty determining the trick of the Western monetary centres' success." Efforts consist of more English-speaking restaurants and services and the structure of numerous new office complex in Tokyo, however more powerful stimuli such as lower taxes have been overlooked and a relative hostility to financing stays widespread in Japan. Tokyo emerged as a significant monetary centre in the 1980s as the Japanese economy ended up being one of the largest in the world.:1 As a monetary centre, Tokyo has excellent relate to New york city City and London. Some also appear as RFCs in numerous lists, particularly Hong Kong, and Singapore. They also appear on a lot of lists of major tax sanctuaries, and on lists https://www.businesswire.com/news/home/20191008005127/en/Wesley-Financial-Group-Relieves-375-Consumers-6.7 of the largest Channel and Sink OFCs in the world. Amsterdam. Amsterdam is well known for the size of its pension fund market. It is also a centre for banking and trading activities. Amsterdam was a popular monetary centre in Europe in the 17th and 18th centuries and several of the innovations established there were carried to London.:24 In June 2017, a study published in ranked the Netherlands as the world's biggest Channel OFC, a term usage to explain the re-routing of fund flows to tax havens. Dublin. Dublin (through its International Financial Solutions Centre, "IFSC"), is a specialised financial services centre with a concentrate on fund administration and domiciling, fund management, custodial activities and airplane leasing. It is the biggest securitisation area in the EU-27, and the second biggest residence for mutual fund, particularly alternative investment funds, after Luxembourg. A number of the funds domiciled and managed in Dublin are at the direction of investment supervisors in bigger Property Management jurisdictions such as London, Frankfurt, New York and Luxembourg.:56 Dublin's innovative BEPS tax tools, for instance the double Irish, the single malt, and the capital allowances for intangible assets (" CAIA") tools, have led the economist Gabriel Zucman to evaluate Ireland to be the largest corporate tax sanctuary by virtue of its usage as a conduit OFC. What Credit Score Is Needed To Finance A Car Things To Know Before You Buy

Luxembourg Click here for info is a specialised monetary services centre that is the biggest location for financial investment fund domiciliation in Europe, and second on the planet after the United States. Numerous of the funds domiciled in Luxembourg are handled in London.:56 Luxembourg is the leading personal banking centre in the Eurozone and the biggest hostage reinsurance centre in Europe. How old of a car will a bank finance. 143 banks from 28 various nations are developed in Luxembourg. The country is also the third biggest renminbi centre in the world by numbers, in particular activities such as deposits, loans, bond listing and mutual fund. 3 of the largest Chinese banks have their European hub in Luxembourg (ICBC, Bank of China, China Building And Construction Bank). With its strong links with London, Singapore has established into the Asia area's largest centre for forex and product trading, in addition to a growing wealth management center. Aside from Tokyo, it is among the main centres for set earnings trading in Asia. Nevertheless, the marketplace capitalisation of its stock market has actually been falling since 2014 and a number of major companies plan to delist. Zurich. Zurich is a substantial centre for banking, asset management consisting of provision of alternative financial investment products, and insurance coverage. Given that Switzerland is not a member of the European Union, Zurich is not directly based on EU guideline. They are certainly significant RFCs. Frankfurt. Frankfurt brings in many foreign banks which preserve offices in the city. It is the seat of Deutsche Brse, among the leading stock exchanges and derivatives markets operators, and the European Reserve Bank, which sets the monetary policy for the single European currency, the euro; in addition, in 2014 the European Central Bank took over responsibility for banking supervision for the 18 nations which form the Eurozone. It is likewise the seat of Deutsche Bundesbank, the German central bank, as well as of EIOPA, the EU's supervisory authority for insurance coverages and occupational pension systems.

All about What Basic Principle Of Finance Can Be Applied To The Valuation Of Any Investment Asset?

Berlin held the position during the intervening period, focusing on lending to European nations while London focused on lending to the Americas and Asia. Bolsa de Madrid. Madrid's stock exchange is the world's second-largest in variety of listed companies. Madrid. Madrid is the head office to the Spanish business Bolsas y Mercados Espaoles, which owns the four stock exchanges in Spain, the largest being the Bolsa de Madrid. What was the reconstruction finance corporation. Trading of equities, derivatives and fixed income securities are connected through the Madrid-based electronic Spanish Stock exchange Affiliation System (SIBE), handling more than 90% of all financial deals. Madrid ranks 4th in European equities market capitalisation, and Madrid's stock market is second in regards to number of noted companies, just behind New York Stock Exchange (NYSE plus NASDAQ). Loan terms are going to vary by loan provider. Much shorter loan terms suggest you pay off the debt earlier, and most likely pay less interest, but longer loan terms guarantee your monthly payment is lower and more budget friendly. While you may pay somewhat more interest over the long term, numerous homeowners choose a 120-month term or longer to make sure payments remain within their budget. Yes. Some of the independent roofing specialists in the Owens Corning Roofer Network offer payment plans to assist make roof replacement costs Check over here more budget-friendly. Payment strategies differ according to requirements, rate of interest and terms, so it is very important to ask the roofing professional you have in mind for more information. If it's because of a weather-related occasion, then homeowner's insurance protection may apply. However if you're simply seeking to change it since of age or to up its resale worth, house owner's insurance coverage likely wouldn't assist with the cost. * APR might differ based upon loan quantity, term, and your credit profile. Funding is independent of Owens Corning and not all candidates might qualify. May 21, 2020 Things are expensive and that includes roofing repair work and replacements. With a typical cost of $9,500, it's simple to believe a roof replacement is out of the budget. However, there are many methods in which you can conserve or utilize funding to cover the expense of changing your house's roofing system. Simply have a look listed below: Before going straight to the bank ant getting a loan, make certain you do all you can to limit just how much money you borrow with these steps: Instead of browsing, get digital quotes from a couple of roof suppliers. Costs differ widely throughout companies, so putting in the Click here time to digitally shop around could keep money in your wallet at the end of your search. Examine This Report about How Long Can You Finance A Boat For

In between metal or another higher-end material and asphalt, a roofing replaced with asphalt material is a lot more spending plan friendly. If the option to change your roofing system is "even if", try waiting until the fall and winter season to replace it. As the summer season months are prime time for roofing system replacements, you could get a good deal come October when need is lower (Which of these is the best description of personal finance). After taking steps to reduce the overall roofing system replacement costs will, next on the list is funding. If you do not have all the money upfront to pay for the replacement, you'll need to go with a financing alternative to pay for the products and labor. Insurer will normally cover repair work if the roof was damaged by storm, fire, and/or left. If your house's roofing was harmed by any of these components and not simply by normal wear and tear call your insurance agent to talk about the payment procedure. If you're dealing with a roof company, you will likely have the ability to use a payment plan to assist with the cost of the roofing replacement. Depending on how long it requires to settle the cost of your replacement, your payments could last months to several years. Just make certain you review the interest rate before you sign! A house equity loan can be a great way to assist spend for your house's roof replacement. In working with your bank or cooperative credit union, you can always take out a personal loan to cover the expense of a new roof. You will easily have the ability to obtain the quantity to cover the roofing repair work expenses, and none of your valuables will be endangered with this kind of loan. Have questions on how we can help you fund your new roofing system? We are here to help! Provide us a call, and one of professionals will deal with you to produce a financing prepare for your roofing replacement.. Not known Facts About How To Finance An Investment Property

You have actually done the research, weighed your alternatives, and lastly chosen the perfect new roofing for your house. Now comes the next action: financing your new roof. Selecting the best roof for your house is a crucial action in maintaining your home's charm and toughness. Consequently, so is roof funding. A brand-new roofing system can be expensive, and it can be overwhelming to figure out how to pay for all of the products and setup. Fortunately, you don't need to go about the procedure of roof financing alone. Today there are numerous various alternatives for loans, rebates, and others methods to obtain roof financing. This includes roofing system funding. Homeowner with excellent credit and restricted house equity what happens to your timeshare when you die get approved for this loan. Banks and other certified loan providers make these loans from their own funds, and FHA guarantees the lending institution versus a possible loss. This consists of brand-new roofs, in addition to improvements to high-end products such as swimming pools or outdoor fire locations. Inspect out the program's website for more details about roofing system funding. If you are funding a new roofing system that is energy effective, be sure to have a look at the Database of State Rewards for Renewable Energy (DSIRE). This website details state, local, utility, and federal rewards for making energy effective enhancements to your home and can help you in the roofing system financing procedure. There are a couple of different methods to handle your roofing financing. @ i, Stockphoto. com/ jamsi If you receive a new no-interest credit card, you may consider utilizing it for your roofing financing. Property owners should prevent charging anything else to this card, and separate the expense into 12 month-to-month payments. If you are arranged and mindful, this is a solid choice for financing a new roofing. A House Equity Line of Credit (HELOC) is a line of credit that uses an owner's home as security. It is normally just utilized for large expenditures, like medical bills and necessary home enhancements. How What Is A Warrant In Finance can Save You Time, Stress, and Money.

Loans and HELOC for roofing funding are strong choices, but the best choice for roofing financing is constantly drawing from your savings. If you understand that you will need a brand-new roofing system in a couple of years, begin putting away $75 - $100 each month. This will assist when it's time to pay the large roofing system costs. Even having the ability to pay a quarter or a third of your roofing system's total cost with cash from your savings will make a distinction in paying for your brand-new roofing system - Which of these is the best description of personal finance. Yes, you can fund a new roof and it may be simpler than you believe to qualify. If you have excellent to exceptional credit and equity in your house you can use a Home Equity Loan. House Equity loans allow you to use your house as security and obtain against its favorable equity. If you do not have equity in your house or have credit obstacles you should think about a personal loan or financing choices offered by the roof or construction company. A little later we'll go into more detail about the different financing choices offered for a new roof. At this moment, you would've ideally settled your first mortgage completely, or at the really least made, constant, timely payments. Moving on, there are some new numbers to which you must pay extra attention to. Second home loan rate of interest on typical tend to be about a quarter of an indicate a half a point higher than the rate of interest on first home mortgages. You'll have to prove to the bank that you can cover both your very first and second home loans with cash to spare. In the days before the Great Recession's housing crisis, it was much easier to leverage a very first house purchase to finance a second house. In the grand scheme of things, though, the interest on your home mortgage is just a part of the general view of things. Bear in mind that down payments on 2nd home loans tend to range from 10% to more than 20%. The tax implications are greatly different when you're leasing out your old home, as opposed to keeping it as one of 2 personal houses. If you opt for the latter, the interest on your second home loan is tax-deductible. But, if you're renting out your first home and creating company income from it for 14 or more music city grand prix date days annually, you won't be eligible to deduct all of the mortgage interest on that second home. With that stated, there are a variety of aspects that enter into being a landlord. In addition to complying with regional proprietor laws, you could face other prospective headaches. You likewise may need to react to a water leak or frozen pipe in the middle of the night. Naturally, there are fundamental expenditures associated with these situations. Some experts approximate you can expect to invest 1% of the purchase rate in upkeep costs each year. Furthermore, you can turn to the "square-foot guideline." This standard suggests you save $1 for every square foot of the residential or commercial property to cover annual maintenance expenses - The trend in campaign finance law over time has been toward which the following?. The rate you spend for this convenience could be high, though. A monetary consultant who's versed in house expenses and home loans can assist you determine if this venture is successful or not. Scoring a second mortgage may be harder than getting one considering that you may have substantial brand-new debt if you have not paid off your very first mortgage. A good genuine estate representative in your area can help you run the numbers to offer you an estimate of what you can expect. It's not difficult to get a loan with a lower credit report. But on average, a credit rating of around 725 to 750 is expected from applicants for second mortgages. In basic, loan providers don't want your financial obligation (including a second home loan) to reach higher than 36% of your month-to-month income prior to taxes. This is what accounts for your personal debt-to-income (DTI) ratio. The process does not end when you approve a new mortgage. Our closing expenses calculator can give you a much better glance of what to expect when you seal the offer. In addition, an excellent realty agent can offer vital insight into aspects like neighborhood safety, school districts, facilities, market value and other regional elements you 'd desire to think about before spending cash for your new house. Your agent can likewise provide you some advice on particular aspects of local home that might help it increase in worth.

All of it depends upon what you can pay for to pay each month, though 15-year mortgages featured lower interest rates than their 30-year counterparts. If you're purchasing your 2nd home before you retire, a strong case can be produced the 30-year payment plan so there is less of a damage in your budget each month. However, you'll pay more in interest with a 30-year home loan than a 15-year home loan. Remember that receiving a second home mortgage might require you to refinance your first home mortgage to minimize the regular monthly payments on your first home. It's also possible to secure a home equity loan and put it toward a deposit on a home mortgage for your second house, which will decrease the mortgage amount on your second house. In many cases, home equity loan interest may be tax deductible. A customer's credit is just as essential in a 2nd home mortgage as it is in the very first. Lenders want to see a positive payment history and beneficial credit report. Most lenders prefer applicants with ratings above 700, but some will go as low as 620. Crucial is the credit history behind ball game. Bankruptcies, late mortgage payments and high charge card balances are all danger aspects that decrease the probability that a lender approves the second home loan. Lenders want to see dependable, continual earnings sources, and the applicant needs to prove these sources will continue for at least three years. In addition, lenders desire a healthy debt-to-income ratio on 2nd home mortgages just as much as on the very first and choose a ratio of no greater than 28 percent. For instance, a buyer who makes $10,000 each month can't permit his regular monthly financial obligation responsibilities to surpass $2,800 per month. Lenders choose liquid possessions, such as savings account funds, and wish to see adequate cash on hand to prove that the consumer can cover numerous months of mortgage, insurance coverage and tax payments on his brand-new loan (What is a cd in finance). In addition, the customer requires to show he has sufficient money on hand to cover all closing expenses. How How To Fight Lease Finance Group can Save You Time, Stress, and Money.

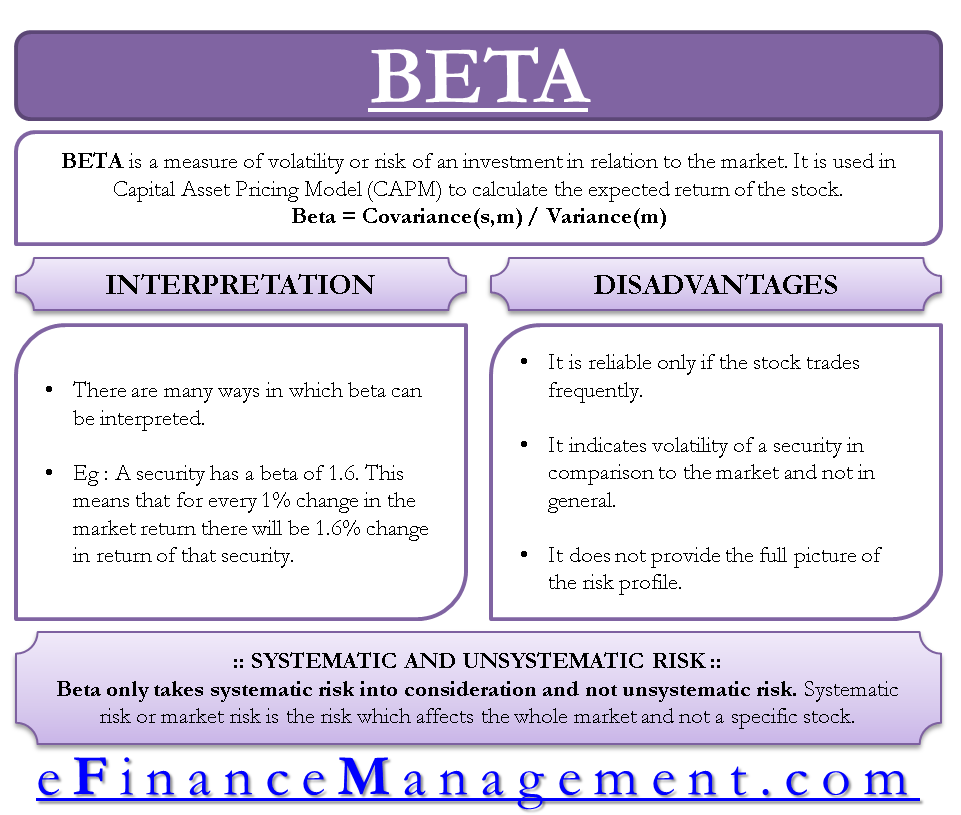

The total amount financed can't go beyond the market worth of the residential or commercial property. If it does, the loan provider can need a bigger deposit or reject the loan. If you imagine owning your very own mountain getaway cabin or ocean-side condominium retreat, you're not alone. And for excellent reason. Owning http://caidenkhrr254.raidersfanteamshop.com/some-known-questions-about-how-to-finance-a-rental-property a villa is a luxury that can also possibly end up being a good financial investment as home worths increase. If you're wondering how you may make that a dream a reality, you're not alone there either. Lots of potential villa owners question about funding a second home. Here's a take a look at what you require to understand about financing yours. Getaway homes and rental houses are financed differently. So before buying your brand-new house away from house, you'll need to find out how yours will be categorized. If it's any closer to your primary house, you'll have a difficult time describing that to your loan officer. Having a trip residential or commercial property that near to your primary home can be a sign that the intent of your villa is to rent it rather than for personal use, which would certify the home under a different loan type. If you do plan to lease your holiday home, it'll be categorized as an investment property, which has various guidelines than a holiday house or primary house, as we'll go over below. With a second house comes a 2nd home loan, and receiving 2 mortgages is a challenge not every buyer can conquer. Compared to loans for primary houses, loans for villa normally have slightly higher rates of interest, and loan providers might require a higher credit rating along with a bigger deposit. For instance, a primary residence allows for deposits as low as 3% for conventional loans. But for a villa, you might need 10 20%. With these kinds of loans, it's also crucial to bear in mind that renting your holiday trip while you're not using it might breach the terms of your loan. With a financial investment residential or commercial property, you'll likely pay a higher rates of interest than those for main houses and villa. Your loan provider may also request an equivalent rent schedule included with your appraisal. But fortunately is that your loan provider will think about a part of the awaited rent as income, which might help you certify for a loan that you otherwise would not without that added income. And obviously you'll be able to offset your costs with the wesley financial group cost regular rental earnings. If you have enough equity in your house, and it makes monetary sense to refinance at the current rate, you may be able to get the cash to purchase your vacation home by doing a cash-out re-finance. A squander re-finance is where you replace your current loan with new home mortgage loan for a bigger amount than the existing quantity, and keep the distinction in between the 2 loans in cash. Just include the quantity of cash you 'd desire to secure under the Advanced Options. Another alternative for those with significant equity in their homes is a house equity line of credit (HELOC). A HELOC is a revolving credit line that lets you obtain against the equity in your house. Similar to a charge card, a HELOC gives you a credit limitation and lets you withdraw the funds as you need them. This is an excellent option if you wish to prevent refinancing the home mortgage on your main home. You would keep your first mortgage with its current rates of interest, and take out a different HELOC loan with different terms. If you can receive a 2nd loan as laid out above, or if you've already paid off your very first mortgage, you can get a new loan for your holiday house. This alternative would assist you avoid re-financing your existing loan, so if you have a lower rate secured, you can keep it that method. Financing a getaway house can be costly, and expenses can add up quicker than you believe. Going in on a trip home with buddies or family can make really buying one more possible. Not figured out by the market rate of interest, is chosen by the reserve banks. Can not be utilized in figuring out present worth. Can be utilized in identifying the present worth of the future capital. Based upon the Market Learn here and concentrating on the Lending institution's perspective Focusing on the Financier's perspective Impacted by Demand and supply in supply in the economy. Not Affected by Demand and supply in supply in the economy. After taking a Continue reading look at the above information, we can state that Discount Rate vs Interest Rate are two different principles. A discount rate is a more comprehensive idea of Finance which is having multi-definitions and multi-usage. In many cases, you need to pay to borrow cash then it is a direct financial cost. In other cases, when you invest cash in a financial investment, and the invested cash can not be made use of in anything else, then there is an chance cost. Discount Rate Rates vs Rate Of Interest both relate to the cost of cash but in a various method. If you have an interest in Finance and wish to operate in the Financial Sector in the future, then you ought to know the difference between Rate of interest and Discount rate. This has a been a guide to the top distinction between Discount Rate vs Rates Of Interest. In financing, the discount rate has two essential meanings. First, a discount rate belongs of the computation of present worth when doing wesley mutual, llc a reduced capital analysis, and second, the discount rate is the rate of interest the Federal Reserve charges on loans offered to banks through the Fed's discount window loan process - How to finance a home addition. The first meaning of the discount rate is an important element of the affordable money flow computation, a formula that identifies how much a series of future money flows is worth as a single lump amount worth today. For financiers, this estimation can be an effective tool for valuing businesses or other investments with predictable profits and capital. The business is steady, constant, and predictable. This business, comparable to lots of blue chip stocks, is a prime prospect for a reduced capital analysis. If we can forecast the company's profits out into the future, we can use the reduced cash flow to approximate what that business's appraisal must be today. Which of these arguments might be used by someone who supports strict campaign finance laws?. Unfortunately, this procedure is not as basic as just accumulating the capital numbers and concerning a worth. That's where the discount rate enters the picture. Money circulation tomorrow is unworthy as much as it is today. We can thank inflation for that reality.

Second, there's uncertainty in any forecast of the future. We simply do not know what will take place, including an unanticipated decrease in a company's earnings. Money today has no such uncertainty; it is what it is. Since capital in the future brings a risk that cash today does not, we must mark down future capital to compensate us for the danger we take in waiting to get it. These 2 elements-- the time value of money and unpredictability risk-- combine to form the theoretical basis for the discount rate. A higher discount rate implies greater unpredictability, the lower the present worth of our future cash circulation. Those "overlays" can avoid you from borrowing, however other banks may utilize different guidelines. It's another reason why it pays to go shopping aroundyou requirement to find a lending institution with competitive costs, and you require to discover a lender who will accommodate your needs. Buying a home may be the biggest financial investment you make in your life, but made homes are typically more affordable than site-built houses. They can make own a home available, specifically for customers with lower incomes and those who reside in rural areas where contractors and products are not readily offered. Produced homes are a clever option for house owners trying to find a recently built contemporary home with an inexpensive home loan payment. While the term "mobile house" is still utilized widely, these single, double and triple-wide premade houses are now referred to as manufactured houses. Funding a produced house or any other kind of home is challenging, however it can be especially tough for a brand-new house owner. A 20% deposit is no longer common. Lots of public and private companies help purchasers who have less than 5% of a house's cost to put down. There are numerous obligations of owning a home that brand-new purchasers should recognize with, and they apply to produced homes too. The biggest expense, obviously, will be purchasing and financing a mobile or manufactured home. Financing is various than for a basic home mortgage, but different programs can make it much easier to qualify. The most significant difference is that loans for mobile and manufactured homes are just for the house itself, not the land it sits upon. The park or community owns the land and leases it to house owners. Called a goods loan, it's a home-only loan and is technically not a realty loan. It's a personal home loan, and is also readily available if you already own the land and require to borrow money to buy the physical home. In reality, it can be much simpler to get financing for a manufactured home than for a standard frame or block home. Financing terms depend upon the loan provider, cancel timeshare legally however the minimum credit report for the choices we go over listed below range from 580-650. Scores higher than 650 might get somewhat much better terms. Ratings lower than 580 may not get approved for a loan at all. Goods loans for manufactured homes are often smaller than standard home loans since you're not buying the land. This can make financing easier for some people due to the fact that they're obtaining less money. Nevertheless, the payment durations are shorter 15 or 20 years which could lead to greater monthly payments. Another downside is that interest rates can be greater on effects loans. A study by the Consumer Financial Protection Bureau discovered that the annual portion rate, or APR, was 1. 5% higher on chattel loans than basic home loans. Loan processing charges, nevertheless, were 40-50% lower. If you're considering buying a produced, mobile or modular house, it is essential to understand the differences in between them. Pricing options vary, as do how they're constructed and installed, and security requirements required in their building and construction, amongst other things. Some loans might be easier to get for some kinds of these homes. Factory-built homes made prior to June 15, 1976, prior to policies Hop over to this website required specific security standards.

Factory-built after June 15, 1976 and based on federal safety requirements embeded in 1974, referred to as the HUD Code. Produced homes are constructed on a long-term metal chassis and can be moved after installation, but that can interfere with funding. These factory-built houses are put together on-site. They need to satisfy the exact same local building codes as site-built homes. They're usually installed on a concrete foundation. Loans are typically simpler to get for modular homes since they hold their worth and appreciate more than the other two. When you've decided what type of manufactured house you desire, you'll require to determine how to finance it. Leasing land could make you qualified for less loans. Buying a double-wide house that costs $100,000 or more isn't allowed in an FHA loan. Maximum loan quantities vary by the type of house bought. Not only must you compare the type of loan, however see how fees and rates of interest vary amongst lenders. Here are four broad funding alternatives: If you own the land under your produced home, you remain in luck. Banks, cooperative credit union and other lending institutions typically need you to own the land in order to get a home loan. In this case, funding a made house is relatively similar to funding a traditional home. Our How To Finance A Car Through A Bank Statements

5% with an FHA loan), and income that is roughly 3 times the mortgage. If you don't believe you have the minimum credit score needed, you can start working to improve your credit report. Online credit therapy from In, Charge Debt Solutions can assist. In, Charge is a nonprofit credit counseling agency that supplies a free picture of your credit report. It can assist you create a repayment plan such as a debt management program. In addition to improving your credit history, owning the land you wish to put a made house on can make being authorized for a loan easier. If you do not plan on purchasing land for your manufactured home, you can still finance the purchase with a bank or credit union loan provider, or possibly through aid from the federal government. These programs are created to assist customers get home loans on manufactured homes, which account for 6% of the U.S. real estate market. That's almost 8 million houses. Real estate support programs started in the New Deal era (1930s) when the government wished to offer much better houses for the rural population. The programs were administered by the USDA due to the fact that the programs were geared towards on-farm housing. The finest thing about a USDA loan (likewise referred to as get rid of timeshare immediately a Rural Advancement loan) is that there is no down payment needed.

The home must meet geographical requirements, but that does not indicate you need to live 20 miles from your closest next-door neighbor. About 97% of the U.S. land mass is USDA loan eligible, an area incorporating 109 million people. Rates of interest change with the market but are typically less than traditional loans. The disadvantage to a USDA loan is a Guarantee Cost of 2% is contributed to the overall loan quantity, and a yearly cost of. 5% gets added to your regular monthly payment. The minimum credit rating to qualify is 640. How old of a car will a bank finance. And unlike standard home mortgages, you can be disqualified for making excessive cash. Inspect with your bank or credit union to see if they can help you with a USDA loan application for a produced loan. No deposit required Can finance 100% of assessed value Minimum credit report required: 650 Should meet geographical requirement: rural area Can't make 115% or more of county's mean income Costs: 2% charge contributed to the overall loan, and. 5% to monthly payment If you surpass the USDA's earnings limit, you ought to consider an FHA loan as they have no wage maximums. The FHA doesn't really offer you cash for a house loan. It insures the loan, which attracts lenders to finance mortgages since they are backed by the federal government. Loan terms are going to differ by lender. Shorter loan terms mean you settle the debt faster, and likely pay less interest, but longer loan terms ensure your regular monthly payment is lower and more budget friendly. While you might pay slightly more interest over the long run, numerous homeowners choose a 120-month term or longer to ensure payments stay within their budget plan. Yes. A few of the independent roofer in the Owens Corning Roofer Network deal payment plans to help make roofing system replacement costs more affordable. Payment plans differ according to requirements, rates of interest and example letter to cancel timeshare terms, so it is necessary to ask the roofer you have in mind for more details. If it's because of a weather-related occasion, then house owner's insurance protection may use. However if you're just wanting to change it because of age or to up its resale value, homeowner's insurance likely wouldn't assist with the cost. * APR might vary based on loan amount, term, and your credit profile. Financing is independent of Owens Corning and not all applicants may qualify. May 21, 2020 Things are costly which consists of roofing repairs and replacements. With an average price of $9,500, it's simple to think a roofing replacement is out of the budget plan. However, there are lots of ways in which you can conserve or use funding to cover the cost of changing your home's roof. Simply have a look below: Before going straight to the bank ant taking out a loan, ensure you do all you can to limit just how much money you borrow with these steps: Rather of window shopping, get digital quotes from a few roofing suppliers. Costs vary commonly across business, so making the effort to digitally go shopping around might keep cash in your wallet at the end of your search. The 10-Minute Rule for What Is The Difference In Perspective Between Finance And Accounting?

Between metal or another higher-end product and asphalt, a roof replaced with asphalt material is a lot more budget plan friendly. If the choice to change your roof is "even if", attempt waiting till the fall and winter season months to replace it. As the summertime are bluegreen timeshare cancellation policy prime-time television for roof replacements, you could get a good deal come October when demand is lower (What is a consumer finance account). After taking steps to lower the overall roofing system replacement expense will, next on the list is financing. If you do not have all the money upfront to pay for the replacement, you'll need to go with a finance option to spend for the materials and labor. Insurance provider will normally cover repairs if the roof was damaged by storm, fire, and/or left. If your house's roofing was damaged by any of these components and not simply by normal wear and tear call your insurance coverage agent to talk about the payment procedure. If you're dealing with a roofing company, you will likely be able to use a payment plan to assist with the cost of the roofing replacement. Depending upon how long it takes to pay off the expense of your replacement, your payments might last months to a number of years. Simply ensure you evaluate the rate of interest before you sign! A home equity loan can be a great way to assist spend for your house's roofing system replacement. In working with your bank or cooperative credit union, you can always get a personal loan to cover the expense of a brand-new roofing system. You will easily be able to obtain the total up to cover the roofing repair work expenses, and none of your valuables will be threatened with this kind of loan. Have questions on how we can assist you fund your brand-new roofing system? We are here to help! Give us a call, and one of specialists will deal with you to create a financing prepare for your roofing system replacement.. The Ultimate Guide To What Does Etf Stand For In Finance

You have actually done the research, weighed your alternatives, and lastly picked the best brand-new roofing system for your home. Now comes the next step: financing your new roofing system. Selecting the perfect roof for your house is an essential action in keeping your house's appeal and sturdiness. Consequently, so is roof financing. A new roofing can be costly, and it can be frustrating to figure out how to spend for all of the materials and setup. Fortunately, you do not have to go about the procedure of roof financing alone. Today there are several various choices for loans, rebates, and others methods to acquire roof financing. This consists of roof funding. Residential or commercial property owners with great credit and https://pbase.com/topics/patric60el/pxipvwx936 restricted house equity get approved for this loan. Banks and other certified loan providers make these loans from their own funds, and FHA guarantees the lending institution versus a possible loss. This includes brand-new roofing systems, along with enhancements to luxury items such as pool or outdoor fire places. Have a look at the program's website for more info about roof funding. If you are financing a new roof that is energy efficient, be sure to have a look at the Database of State Rewards for Renewable Energy (DSIRE). This site details state, regional, utility, and federal rewards for making energy effective improvements to your house and can assist you in the roofing system financing procedure. There are a few different ways to manage your roofing system financing. @ i, Stockphoto. com/ jamsi If you receive a new no-interest credit card, you may consider utilizing it for your roofing system financing. Property owners must avoid charging anything else to this card, and break up the expense into 12 monthly payments. If you are organized and cautious, this is a strong alternative for financing a brand-new roofing system. A Home Equity Credit Line (HELOC) is a credit line that utilizes an owner's home as security. It is usually just utilized for big costs, like medical costs and essential home improvements. 6 Simple Techniques For How To Cite Yahoo Finance Apa

Loans and HELOC for roofing system funding are strong choices, but the very best choice for roofing financing is always drawing from your savings. If you know that you will need a new roof in a couple of years, begin putting away $75 - $100 every month. This will assist when it's time to pay the large roofing system expense. Even having the ability to pay a quarter or a third of your roofing's overall rate with money from your savings will make a difference in spending for your new roofing system - How to finance a home addition. Yes, you can fund a brand-new roofing and it may be simpler than you think to certify. If you have excellent to outstanding credit and equity in your house you can use a House Equity Loan. Home Equity loans allow you to use your home as collateral and obtain versus its positive equity. If you do not have equity in your house or have credit challenges you need to think about a personal loan or financing options provided by the roof or building and construction company. A little in the future we'll go into more detail about the numerous funding choices available for a brand-new roofing. At this point, you would've ideally settled your first mortgage totally, or at least made, consistent, timely payments. Moving forward, there are some new numbers to which you ought to pay extra attention to. 2nd home mortgage rates of interest on average tend to be about a quarter of a point to a half a point greater than the rate of interest on very first home mortgages. You'll have to show to the bank that you can cover both your very first and 2nd home mortgages with cash to spare. In the days before the Great Economic crisis's real estate crisis, it was simpler to leverage a very first house purchase to fund a second house. In the grand scheme of things, though, the interest on your home mortgage is just a part of the general view of things. Remember that deposits on 2nd home loans tend to range from 10% to more than 20%. The tax ramifications are significantly various when you're leasing your old house, instead of keeping it as one of 2 personal houses. If you go with the latter, about timeshares the interest on your 2nd home loan is tax-deductible. However, if you're renting your very first house and generating business earnings from it for 14 or more days annually, you won't be eligible to subtract all of the home loan interest on that second home. With that stated, there are a number of components that go into being a landlord. In addition to abiding by regional landlord laws, you might deal with other prospective headaches. You also may have to react to a water leakage or frozen pipe in the middle of the night. Obviously, there are intrinsic costs related to these scenarios. Some experts estimate you can anticipate to invest 1% of the purchase cost in maintenance costs each year. Additionally, you can resort to the "square-foot rule." This guideline recommends you save $1 for every square foot of the property to cover yearly upkeep expenses - How old of an rv can you finance.

The price you spend for this comfort might be steep, though. A financial advisor who's versed in home costs and mortgages can assist you determine if this endeavor pays or not. Scoring a second home loan might be harder than acquiring one considering that you may have significant brand-new debt if you haven't settled your very first mortgage. An excellent property agent in your location can help you run the numbers to give you a price quote of what you can anticipate. It's not impossible to get a loan with a lower credit history. But typically, a credit rating of around 725 to 750 is anticipated from candidates for 2nd home mortgages. In general, lenders don't want your financial obligation (including a 2nd home mortgage) to reach greater than 36% of your regular monthly earnings prior to taxes. This is what accounts for your personal debt-to-income (DTI) ratio. The procedure doesn't end when you accept a new mortgage. Our closing expenses calculator can give you a better look of what to anticipate when you seal the deal. In addition, a great real estate representative can offer important insight into aspects like area security, school districts, features, market costs and other regional aspects you 'd wish to consider before shelling out cash for your new home. Your representative can also give you some guidance on particular elements of local property that may help it increase in value. All of it depends upon what you can manage to pay every month, though 15-year mortgages come with lower rate of interest than their 30-year counterparts. If you're purchasing your 2nd home prior to you retire, a strong case can be produced the 30-year payment strategy so there is less of a dent in your spending plan monthly. Nevertheless, you'll pay more in interest with a 30-year mortgage than a 15-year home loan. Bear in mind that getting approved for a second mortgage might need you to re-finance your very first home loan to minimize the regular monthly payments on your very first house. It's likewise possible to take out a home equity loan and put it toward a down payment on a mortgage for your 2nd house, which will reduce the home loan quantity on your second home. Sometimes, home equity loan interest may be tax deductible. A consumer's credit is just as important in a 2nd mortgage as it is in the first. Lenders wish to see a favorable payment history and favorable credit rating. A lot of lending institutions choose applicants with ratings above 700, however some will go as low as 620. Essential is the credit history behind ball game. Personal bankruptcies, late home mortgage payments and high charge https://israelsvkf455.wordpress.com/2022/04/28/some-known-factual-statements-about-how-to-import-stock-prices-into-excel-from-yahoo-finance/ card balances are all threat factors that decrease the likelihood that a lender approves the 2nd home loan. Lenders want to see trusted, consistent income sources, and the candidate requires to prove these sources will continue for a minimum of 3 years. In addition, lenders want a healthy debt-to-income ratio on second home mortgages just as much as on the very first and prefer a ratio of no greater than 28 percent. For example, a purchaser who makes $10,000 monthly can't allow his month-to-month debt commitments to surpass $2,800 monthly. Lenders choose liquid assets, such as savings account funds, and wish to see enough cash on hand to prove that the consumer can cover several months of home mortgage, insurance and tax payments on his brand-new loan (Which of these arguments might be used by someone who supports strict campaign finance laws?). In addition, the consumer needs to show he has adequate cash on hand to cover all closing expenses. Rumored Buzz on What Basic Principle Of Finance Can Be Applied To The Valuation Of Any Investment Asset?

The overall amount financed can't surpass the marketplace worth of the property. If it does, the loan provider can need a bigger deposit or deny the loan. If you imagine owning your really own mountain vacation cabin or ocean-side apartment retreat, you're not alone. And for good factor. Owning a trip house is a high-end that can likewise possibly end up being a great investment as home values rise. If you're questioning how you may make that a dream a reality, you're not alone there either. Lots of potential villa owners question about funding a 2nd house. Here's a take a look at what you require to learn about financing yours. Trip homes and rental houses are financed in a different way. So before buying your new home far from home, you'll need to determine how yours will be classified. If it's any closer to your main home, you'll have a hard time describing that to your loan officer. Having a getaway residential or commercial property that near your main house can be an indication that the intent of your trip home is to rent it rather than for individual use, which would certify the home under a various loan type. If you do plan to lease your vacation house, it'll be categorized as an investment home, which has various guidelines than a villa or primary residence, as we'll go over below. With a second house comes a second home loan, and certifying for two home mortgages is an obstacle not every purchaser can overcome. Compared to loans for main houses, loans for villa generally have slightly higher rates of interest, and lenders might need a greater credit report as well as a bigger deposit. For example, a main house permits deposits as low as 3% for conventional loans. But for a trip home, you may need 10 20%. With these kinds of loans, it's likewise crucial to bear in mind that renting your holiday getaway while you're not using it might breach the regards to your loan. With an investment property, you'll likely pay a greater rate of interest than those for main residences and vacation homes. Your loan provider may also ask for a comparable rent schedule consisted of with your appraisal. But the bright side is that your lending institution will think about a portion of the anticipated lease as earnings, which might assist you certify for a loan that you otherwise would not without that included income. And of course you'll be able to offset your expenses with the routine rental income. If you have enough equity in your house, and it makes financial sense to refinance at the existing rate, you may have the ability to get the money to purchase your villa by doing a cash-out re-finance. A squander re-finance is where you change your current loan with brand-new mortgage for a bigger amount than the existing amount, and keep the distinction between the 2 loans in money. Simply add the quantity of cash you 'd desire to take out under the Advanced Options. Another choice for those with considerable equity in their houses is a home equity line of credit (HELOC). A HELOC is a revolving line of credit that lets you borrow against the equity in your home. Comparable to a credit card, a HELOC provides you a credit line and lets you withdraw the funds as you need them. This is a good alternative if you want to avoid re-financing the mortgage on your main home. You would keep your very first mortgage with its current rate of interest, and get a different HELOC loan with various terms. If you can get approved for a second loan as laid out above, or if you've already settled your very first home mortgage, you can get a brand-new loan for your villa. This option would assist you avoid re-financing your existing loan, so if you have a lower rate locked in, you Take a look at the site here can keep it that way. Financing a villa can be costly, and costs can accumulate quicker than you believe. Entering on a vacation residential or commercial property with good friends or family can make in fact buying one more possible. |

RSS Feed

RSS Feed